August 2019

|

August 2019 // Volume 57 // Number 4 // Ideas at Work // v57-4iw6

A Model for Youth Financial Education in Extension Involving a Game-Based Approach

Abstract

University of Idaho Extension educators have developed a library of 10 game-based personal finance programs, collectively known as the Northwest Youth Financial Education project, and have made these programs freely available for Extension educators to use. The purpose of this article is to share highlights from an associated train-the-trainer event and the impacts of one of the 10 programs as it has begun to be implemented. The Northwest Youth Financial Education project serves as a model for effective and engaging youth personal finance education that can be easily implemented or replicated in Extension.

Background

Personal finance education for youth has long been considered important by parents, educators, economists, public decision makers, and others (Osteen, Muske, & Jones, 2007; Uhl, 1970). Yet many state Extension systems struggle to provide sufficient personal finance programming to meet local needs.

Research on effective financial education has indicated that opportunities for practical application, or "learning by doing," are vital (Carlson, 2014; Franklin, 2015; O'Neill, 2008) and that youths respond well to digital games in the educational process (deCos, 2015; Schuster, 2012). Financial games and simulations have been successfully implemented both in and out of schools (Mosley, 2014; O'Neill, 2008) and offer tremendous flexibility for helping students learn at their own pace (Jones & Chang, 2014). Additionally, incorporating digital games in experiential learning settings allows for trial and error without putting learners at risk (Jones & Chang, 2014). Use of financial games and simulations has been shown to help students gain knowledge, experience, and confidence that transfer to real financial situations and establish a foundation for becoming financially stable adults (Jones & Chang, 2014; Nosal, 2013). Virtual game worlds can make financial topics more engaging to students, and providing the potential to cooperate or compete with friends while learning and playing is becoming a popular way to add social interaction to learning (Hai, 2014; Liu et al., 2011). The vast potential of digital games for delivering cost-effective, financial experiences to highly engaged students is much too strong to ignore (Richards, Williams, Smith, & Thyer, 2015).

Program Description

With support from Northwest Farm Credit Services and CoBank, authors Erickson and Hansen led the creation of the Northwest Youth Financial Education project to help address priority needs in five northwestern states. Following a logic-model-based process, we identified educational priorities through input from an advisory board, surveys, and research. On the basis of the findings, we created a library of 10 youth personal finance educational games (referred to as programs and accessible through the Northwest Youth Financial Education website at www.uidaho.edu/nw-youth-financial-ed), which are designed to be delivered in group settings. Youths have responded exceptionally well to learning personal finance concepts through games, and instructors are often surprised at how easy the programs are to facilitate, even if they do not have content or technological expertise.

Training

We organized a regional training on the Northwest Youth Financial Education programs that was attended by 35 Extension educators, seven advisory board members, and five representatives of the funding organizations, all of whom together represented the five northwestern states. The results of a retrospective evaluation of the training indicated that participants experienced improved confidence for teaching financial topics (Table 1) and high likelihood of using the programs (Table 2).

| Before training | After training | |||||

|---|---|---|---|---|---|---|

| Topic | Very confident | Somewhat confident | Not very confident | Very confident | Somewhat confident | Not very confident |

| Saving and investing | 24% | 58% | 18% | 58% | 39% | 3% |

| Paying for college | 31% | 50% | 19% | 63% | 37% | 0% |

| Credit cards | 33% | 39% | 28% | 76% | 21% | 3% |

| Financial apps | 9% | 27% | 64% | 39% | 55% | 6% |

| Credit scores | 16% | 51% | 33% | 67% | 27% | 6% |

| Program name | Definitely will | Probably will | Maybe | Probably won't | Definitely won't |

|---|---|---|---|---|---|

| Max Learns About Money | 34% | 36% | 21% | 9% | 0% |

| Marlon Monkey Borrows Bananas | 44% | 31% | 16% | 9% | 0% |

| Student Loans | 62% | 21% | 12% | 3% | 0% |

| Teens Credit Card | 55% | 39% | 6% | 0% | 0% |

| Money Ninja Warrior | 35% | 45% | 13% | 7% | 0% |

| Ready for the World | 33% | 36% | 31% | 0% | 0% |

| Night of the Living Debt | 32% | 47% | 21% | 0% | 0% |

| Credit Score Millionaire | 69% | 31% | 0% | 0% | 0% |

Participants were asked whether their training and the Northwest Youth Financial Education programs might make a difference to their local youth audiences. In response, participants shared the following comments:

- "Absolutely. The importance of personal financial management is over-looked in our communities."

- "Yes, great format for reaching today's youth."

- "Yes, valuable, relatable lessons and simple, understandable structure."

- "Yes, attractive, practical, well-designed. . . . Will be easier for youth to grasp concepts and adhere information to their brain."

- "Yes. I have wanted to do this type of education for a long time. This gives me the tools."

Implementation and Example Outcomes

At the time of this writing, 20 educators from eight states had delivered Northwest Youth Financial Education programs in face-to-face settings, and the program had reached over 26,000 individuals through direct programming and private-play sessions.

Data for the Night of the Living Debt game serve to exemplify the success of the individual educational games under the Northwest Youth Financial Education umbrella. In response to the success of the Credit Score Millionaire program (Erickson & Hansen, 2016) and growing demand for credit score education, authors Erickson and Hansen collaborated with author Chamberlin and the New Mexico State University Learning Games Lab to create this free mobile game for iPad tablets. On the basis of the transformational learning model employed by the lab, the entire team collaborated to identify the desired change in game players, the activities necessary for creating that change, and a game design that would engage players in those activities. The game uses cartoonlike zombies as a metaphor for financial payments, with the concept being that zombies and debt have a lot in common in that you might survive if one or two follow you but too many of either can quickly overwhelm you (Figure 1). The content focuses on real-time consequences of financial decisions on credit scores, played out in a fictional game world.

Figure 1.

Night of the Living Debt App—Title Screen

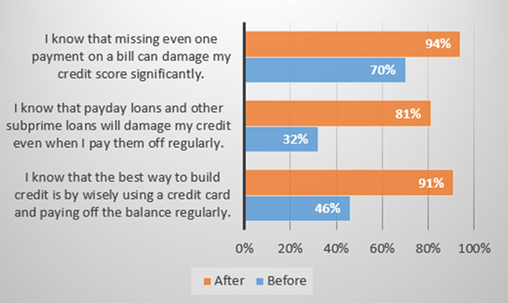

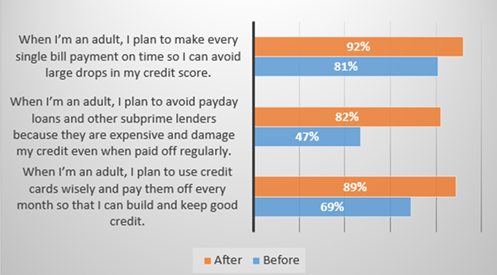

Opt-in iTunes statistics collected prior to the time of this writing indicated that the Night of the Living Debt app had been downloaded 886 times and played individually 7,705 times, with downloads occurring in a variety of countries. The program had been offered face-to-face to over 1,500 Extension program participants, and participant surveys indicated an overall rating of 9 out of 10 for enjoyment and engagement. Data for knowledge gain and intended behavior reported by participants in the face-to-face programming are shown in Figures 2 and 3.

Figure 2.

Night of the Living Debt—Participant Knowledge Gain

Figure 3.

Night of the Living Debt—Participant Intended Behavior

When asked to comment on the overall experience of participating in the game, participants gave positive responses. The following comments are some examples:

- "I really enjoyed it. I learned a lot. I'm going to spend my money more wisely."

- "I'm glad I was here for this lesson."

- "I like it, it is not only fun but also teaches you a lesson."

- "I think this is good, because it teaches us how to save some money so when we are adults, we won't make mistakes to our credit scores."

In a retrospective evaluation, participants were asked to estimate the financial difference that the knowledge they gained from the program might have on them personally. On average, participants reported an estimated $619 that would be saved through sound future financial decisions. With 1,500 face-to-face participants to date at that time, that value equated to $928,500 in estimated clientele savings as a result of the program. And if that estimated figure were applied to all play sessions, including individual downloads/plays, the estimated economic impact of the program at that time could have been about $5.6 million.

Conclusion

Night of the Living Debt and the other Northwest Youth Financial Education programs successfully model scalable, game-based experiential financial education that has resulted in high levels of engagement, knowledge gain, and intended behavior change. These findings suggest that implementing video games designed to change behavior could be considered a "best practice" in Extension, particularly for personal finance education (Nosal, 2013).

References

Carlson, K. (2014). Financial forest: A smart phone app (Unpublished doctoral dissertation). University of Central Florida, Orlando, Florida.

deCos, L. (2015). Opportunity for banks to utilize gamification as a tool to promote financial education to children (Bachelor's thesis, Turku University of Applied Sciences, Turku, Finland). Retrieved from http://www.theseus.fi/handle/10024/90868

Erickson, L., & Hansen, L. (2016). Credit Score Millionaire: An innovative program helps diverse audiences build strong credit scores. Journal of Extension, 54(3), Article 3IAW5. Available at: https://joe.org/joe/2016june/iw5.php

Franklin, D. (2015). Teacher involvement in implementing state personal finance mandates (Doctoral dissertation). Available from ProQuest. (UMI 3717347)

Hai, F. (2014). Next generation financial guidance tool. Retrieved from University of California, Berkeley website: http://xtf.lib.berkeley.edu/reports/TRWebData/accessPages/EECS-2014-69.html

Jones, D. A., & Chang, M. (2014). Pecunia: A life simulation game for finance education. Research & Practice in Technology Enhanced Learning, 9(1).

Liu, C., Franklin, T., Shelor, R., Ozercan, S., Reuter, J., Ye, E., & Moriarty, S. (2011). A learning game for youth financial literacy education in the teen grid of Second Life three-dimensional virtual environment. American Journal of Business Education, 4(7), 1–18.

Mosley, C. L. (2014). A model for collaborative partnership: Virginia Cooperative Extension and the local school system support financial education mandates. Retrieved from the Virginia Tech website: https://vtechworks.lib.vt.edu/handle/10919/51510

Nosal, E. M. (2013). It figures in their future: Assessing the impact of Everfi, a virtual environment, on learning high school personal finance (Doctoral dissertation). Retrieved from http://mars.gmu.edu/xmlui/handle/1920/8759

O'Neill, B. (2008). Financial simulations for young adults: Making the "real world" real. Journal of Extension, 46(6), Article 6TOT4. Available at: https://www.joe.org/joe/2008december/tt4.php

Osteen, S., Muske, G., & Jones, J. (2007). Financial management education: Its role in changing behavior. Journal of Extension, 45(3), Article 3RIB2. Available at: https://www.joe.org/joe/2007june/rb2.php

Richards, K., Williams, J. M., Smith, T. E., & Thyer, B. A. (2015). Financial video games: A financial literacy tool for social workers. International Journal of Social Work, 2(1), 22.

Schuster, E. (2012). Mobile learning and the visual web, oh my! Nutrition education in the 21st century. Journal of Extension, 50(6), Article 6COM1. Available at: https://www.joe.org/joe/2012december/comm1.php

Uhl, J. N. (1970). Survey and evaluation of consumer education programs in the United States. Vol. I: Survey and evaluation of institutional and secondary school consumer education programs. Vol. II: Sourcebook of consumer education programs. Final report. Retrieved from Institute of Education Sciences: http://files.eric.ed.gov/fulltext/ED038549.pdf