October 2018

|

October 2018 // Volume 56 // Number 6 // Research In Brief // v56-6rb8

Use of "the Guidelines" for Financial Record Keeping by Kentucky Small- and Mid-Scale Farmers

Abstract

We describe awareness of the Financial Guidelines for Agricultural Producers ("the Guidelines") and illustrate their use on Kentucky small and mid-size farms. Using survey data we collected in 2016 from 103 farms, we found that 89% of the small- and mid-scale farmers who responded were unaware of the Guidelines and, therefore, did not follow them. Additionally, 75% of the farmers used a single-entry cash-basis accounting system. We consequently suggest the implementation of awareness campaigns, educational strategies, and technical assistance to increase farmers' awareness and usage rates with regard to the Guidelines. We also suggest that there is a need for training on double-entry accrual accounting techniques.

Introduction

Keeping farm records is crucial to farm business success. Farm financial weakness can be one of the most convincing reasons to stop farming. During the farm debt crisis of 1983–1987, the Agricultural Division of the American Bankers Association wrote a report to standardize many aspects of agricultural finances (Farm Financial Standards Council, 2011). The main purpose was to ensure universal accounting standards for farm businesses. In 1989, the Farm Financial Standards Task Force was formed and later created the Financial Guidelines for Agricultural Producers (commonly referred to simply as "the Guidelines"). Fischer and Marsh (2013) indicated that the Guidelines provide standards for formats and contents of financial reports and financial measures (ratios) that can be used across all sectors of agriculture. In 1994 the Farm Financial Standards Task Force changed its name to Farm Financial Standards Council (FFSC). The mission of the FFSC still is to create and promote uniformity and integrity in financial reporting and analysis for agricultural producers.

Although the Guidelines exist, farmers still have the option of following other accounting procedures. For example, they may use the Generally Accepted Accounting Principles (GAAP) or the international accounting procedures that are outlined in International Accounting Standard 41–Agriculture, which most of the world uses (International Accounting Standard, 2017; Marsh & Fischer, 2013). However, the Guidelines call for using accrual adjustment procedures and are said to give a more accurate measure of what is happening financially on a farm (Bergmann, 2012; Internal Revenue Service, 2017). Each accounting technique has its own advantages and disadvantages, and a farmer must determine which method is best for his or her farm (Kurniawan, Mulawarman, & Kamayanti, 2014; Smetanka, 2012). That said, the Guidelines are meant to put farmers at an advantage when it comes to their financial standings (Doehring, 2012).

The Guidelines were created to help farmers maintain their accounts in a more accurate way that takes the specific needs of famers into consideration. Good record keeping leads to good decision making, which in turn leads to a better overall financial standing (Figurek, 2015). In fact, many believe that good record keeping and farm profitability go hand in hand (Dechow, Ge, Larson, & Sloan, 2011; Utegi & Utegi, 2014). Knowing how his or her agribusiness is doing financially enables a farmer to make educated and informed decisions about the business (Doğan, Arslan, & Köksal, 2013; Miller et al., 2010; Vazakidis, Stergios, & Laskaridou, 2010). However, famers or farm accountants often do not use the Guidelines. The difference between Guidelines users and nonusers remains unknown. Research studies in this area are very limited. Therefore, for the study reported here, we had the following objectives:

- Describe characteristics of Kentucky small- and mid-scale farmers.

- Illustrate the levels of awareness about the Guidelines among Kentucky small- and mid-scale farmers.

- Explain various record-keeping techniques used on Kentucky small and mid-size farms.

On the basis of our findings, we suggest a set of recommendations for Extension entities to use to provide assistance aimed at enhancing use of the Guidelines among small- and mid-scale farmers and/or their farm accountants.

Methodology

Our study is based on survey data collected in the summer of 2016. The study is limited to small and mid-size farms that were registered with the Kentucky Department of Agriculture by May 15, 2016, when we started collecting data. The U.S. Department of Agriculture (2013) defines small and mid-size farms as those whose annual gross sales are less than $500,000. At the time we collected data, there were 4,351 such farms registered. We limited our study to small and mid-size farms because Kay, Edwards, and Duffy (2015) and Ricketts and Ricketts (2009) indicated that many of these ventures fail due to lack of appropriate record keeping. We also assumed that small- and mid-scale farmers have limited resources for employing expert accountants.

We randomly selected 650 farms from the database of 4,351 small and mid-size farms. Statistically, this sample represents 15% of the targeted population. According to the sample size calculator developed by Creative Research Systems (2012), this sample represents a confidence level of 95% and a margin of error of 3.55%. According to DataStar (2008), a 3% margin is one of the lowest margins used by survey researchers when 95% confidence level is involved. This means that the sample is a good representation of the population.

We mailed the surveys to the farm owners. We also included on the paper survey a website link to provide an opportunity for respondents to complete the survey online. To stimulate greater response, we offered participants the chance to win one of 10 Visa gift cards of $50 each. We received 103 complete responses, 95 paper based and eight web based, for a 16% response rate. All descriptive statistics reported herein are based on 103 completed responses.

Results

Through the survey, we identified characteristics of the farmers who participated in the study. Descriptive data are presented in Table 1.

| Characteristic | Value |

| Mean age | 49 years |

| Full-time farmer | 34% |

| Married | 79% |

| Farm experience | |

| Less than 1 year | 3% |

| 1–5 years | 29% |

| 5–10 years | 22% |

| 10–20 years | 18% |

| More than 20 years | 28% |

| Education | |

| No high school | 1% |

| High school or equivalent | 9% |

| Some college | 38% |

| 4-year university degree | 34% |

| Some graduate | 17% |

| Gross sales revenue for 2015 | |

| Less than $50,000 | 33% |

| $50,000–$100,000 | 25% |

| $100,000–$250,000 | 37% |

| $250,000–$500,000 | 5% |

| Feelings about farm financial position | |

| Very strong | 11% |

| Moderately strong | 20% |

| Fair | 32% |

| Slightly weak | 20% |

| Very weak | 16% |

| Type of operation | |

| Crops | 32% |

| Livestock | 21% |

| Fresh produce | 18% |

| Farm and ranch | 29% |

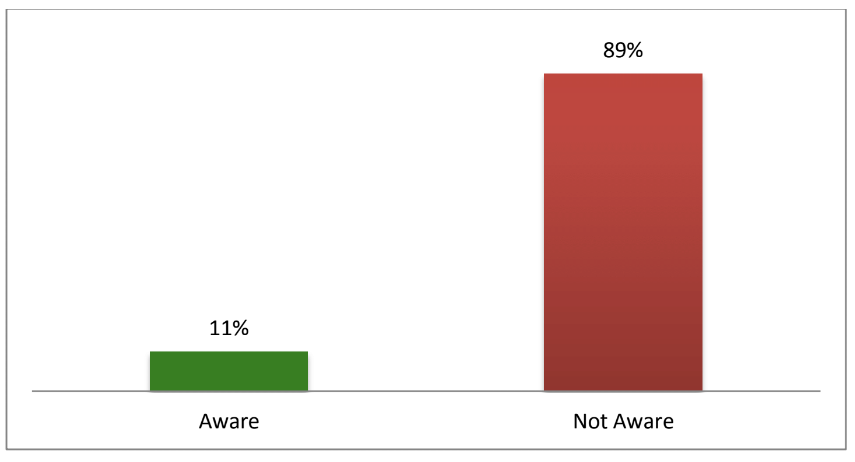

Respondents were told that the Farm Financial Standards Task Force created Financial Guidelines for Agricultural Producers, commonly known as the Guidelines. They were then asked whether they were aware of the Guidelines. Figure 1 illustrates their responses.

Figure 1.

Distribution of Respondents Regarding Awareness of the Guidelines

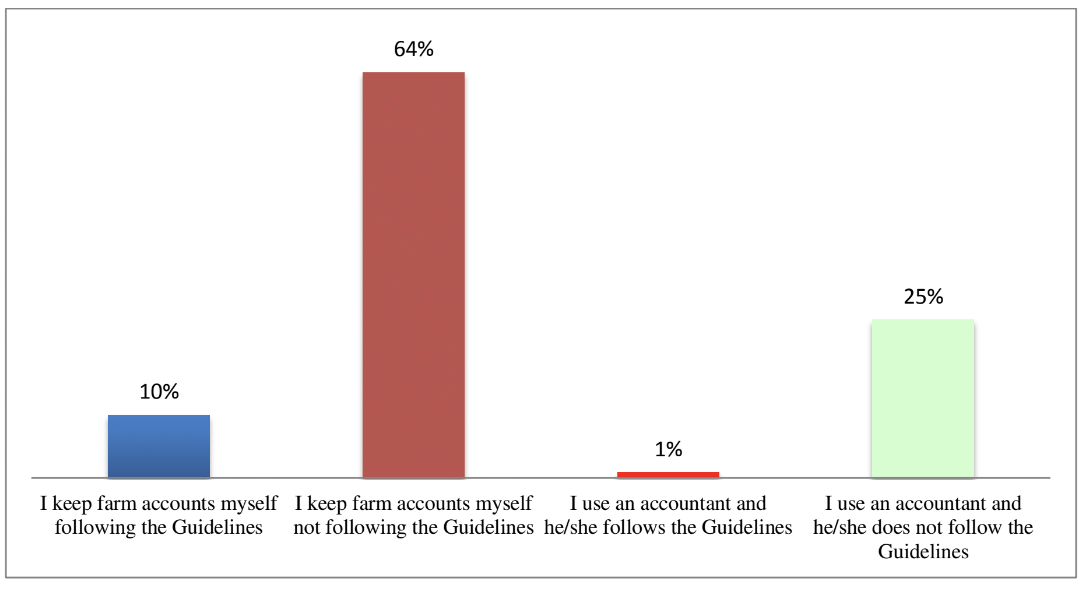

We further asked respondents to choose the most applicable statement in relation to their farm accounting (record-keeping) procedures. Respondents were given four options to choose from. The options were (a) I keep farm accounts myself following the Guidelines, (b) I keep farm accounts myself not following the Guidelines, (c) I use an accountant and he/she follows the Guidelines, and (d) I use an accountant and he/she does not follow the Guidelines. Figure 2 shows the responses to the question.

Figure 2.

Distribution of Respondents Regarding Following the Guidelines in the Farm Accounting System

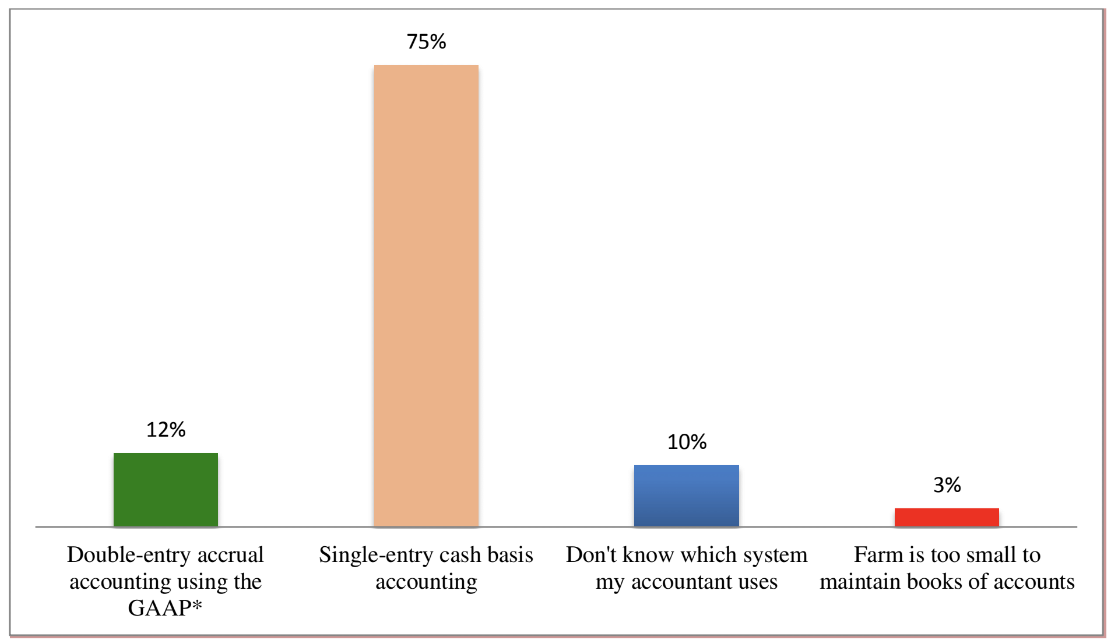

We were interested in identifying accounting systems commonly used by nonusers of the Guidelines. Figure 3 shows a distribution of accounting systems usage.

Figure 3.

Accounting Systems Usage Among Nonfollowers of the Guidelines

*GAAP = Generally Accepted Accounting Principles.

Discussion, Recommendations, and Concluding Remarks

Our results indicate that an average respondent to our study was 49 years old and that the majority of small- and mid-scale Kentucky farmers who responded to the study had been operating their farms for more than 20 years. It is clear that these farmers and ranchers had extensive experience. Extension specialists might find it useful to engage experienced farmers in the process of assisting beginning farmers in improving their record-keeping practices. However, they should keep in mind the fact that the majority of the farmers who responded to our survey (66%) operated their farms on part-time bases. This finding indicates that many small- and mid-scale farm owners work off-farm to complement their farm income. As a result, they might not be available to assist, except when they receive compensation.

Other demographic factors of interest are education level and sales revenue. The study showed that the 51% of small- and mid-scale Kentucky farmers hold a 4-year university degree or a graduate degree. In general, it would be beneficial for the agriculture industry if this number were to increase. According to the U.S. Department of Agriculture (2017), farmers face unique challenges and require education and training to ensure their success. We also report on participants' gross farm sales revenues for 2015. The majority of the respondents (58%) made less than $100,000. It is worth considering whether net farm income for these farmers is economically viable. We suggest that this is one reason many seek off-farm employment (Gillespie & Mishra, 2011).

Insight can be gained by noting respondents' characterizations of the financial statuses of their operations. Responses were based on a 5-point Likert scale (1 = very weak and 5 = very strong). Although the farmers' feelings might be subjective, it appears that the majority of the small- and mid-scale farmers who responded to our study (63%) were at least fairly satisfied by their profession. This finding does not necessarily mean that their satisfaction is derived from sufficient farm income. For example, regardless of farm size, one may feel satisfied by the sustainability of his or her farm assets, liabilities, and owner's equity. Furthermore, those with off-farm income may still feel satisfied by a farm's financial position even when the farm size does not allow for complete economic independence.

With regard to managing farm finances, we found that many of our respondents did so without employing a professional accountant. Although this practice reduces the explicit expenses for a farm, the question is whether the resulting financial statements are (a) understandable, (b) adherent to rules and guidelines, (c) reliable, (d) complete and accurate, and (e) relevant (Wheeling, 2008). Two aspects of our findings may help answer this question. First, as shown in Figure 1, the vast majority of respondents were not aware of the Guidelines and, therefore, may not be keeping effective records. Second, in Figure 3, we report that many of these farmers used a single-entry accounting system. According to the capacity-building organization Village Volunteers (2011), single-entry systems are far easier to understand and use, but they do not offer the same levels of accuracy and complexity that a double-entry system can provide.

The fact that we found a large majority of farmers using a single-entry cash-basis accounting system almost mirrors the findings by Ibendahl, Isaacs, and Trimble (2002) that 66% of farmers in Kentucky used such a system to track cash expenses and were not developing much analysis from their records. Others also have reported that the majority of farmers use a cash-basis approach in their record keeping (Barth, Landsman, Lang, & Williams, 2012; Cohen, Kaimenakis, & Venieris, 2013; Evans, Houston, Peters, & Pratt, 2015). Many farmers feel that cash-basis accounting procedures are easier to follow and allow for a prediction of future income (Curtis, Mcvay, & Whipple, 2014).

Our results also show that that among those respondents who did not follow the Guidelines, only 12% used a double-entry accrual accounting system following the GAAP. This low percentage might be associated with the fact that considerable accounting skills and expertise are required to use a double-entry accrual accounting system (Bosch, Aliberch, & Blandón, 2012). Using methods other than those specifically designed for agriculture accounting can cause some issues when reporting expenses and values. As Bosch et al. (2012) recommended, farmers should follow the Guidelines to avoid these issues. Despite such recommendations, we found that the majority of the farmers we surveyed (89%) were nonusers of the Guidelines.

Overall, our findings suggest that Extension agents and other agricultural educators should provide training on financial record keeping to small- and mid-scale farmers. Providing training on the double-entry accrual accounting system is important because it is the most accurate and complete approach (Kay et al., 2015; Wheeling, 2008). Likewise, developing educational programs to increase awareness of and/or train farmers on how to use the Guidelines would be beneficial. These programs would increase farmers' awareness of the Guidelines and knowledge about accurate and proper record keeping for their operations. We suggest the undertaking of further studies that make a comparison analysis of farm financial positions of Guidelines users and nonusers. We also suggest that researchers in other states conduct studies similar to ours to help establish a basis for a greater understanding of the issue at a national level.

References

Barth, M. E., Landsman, W. R., Lang, M., & Williams, C. (2012). Are IFRS-based and US GAAP-based accounting amounts comparable? Journal of Accounting and Economics, 54(1), 68–93. doi:10.1016/j.jacceco.2012.03.001

Bergmann, A. (2012). The influence of the nature of government accounting and reporting in decision-making: Evidence from Switzerland. Public Money & Management, 32(1), 15–20. doi:10.1080/09540962.2012.643050

Bosch, J. M., Aliberch, A. S., & Blandón, J. G. (2012). A comparative study of difficulties in accounting preparation and judgment in agriculture using fair value and historical cost for biological assets valuation. Revista de Contabilidad, 15(1), 109–142. doi:10.1016/S1138-4891(12)70040-7

Cohen, S., Kaimenakis, N., & Venieris, G. (2013). Reaping the benefits of two worlds: An explanatory study of the cash and the accrual accounting information roles in local governments. Journal of Applied Accounting Research, 14(2), 165–179.

Creative Research Systems. (2012). Sample size calculator. Retrieved from http://www.surveysystem.com/sscalc.htm

Curtis, A., Mcvay, S., & Whipple, B. (2014). The disclosure of non-GAAP earnings information in the presence of transitory gains. Accounting Review, 89(3), 933–958. doi:10.2308/accr-50683

DataStar. (2008). What every researcher should know about statistical significance. Retrieved from http://www.surveystar.com/startips/oct2008.pdf

Dechow, P. M., Ge, W., Larson, C. R., & Sloan, R. G. (2011). Predicting material accounting misstatements. Contemporary Accounting Research, 28(1), 17–82. doi:10.1111/j.1911-3846.2010.01041.x

Doehring, T. A. (2012). Analyzing the profitability of your operation. Retrieved from http://www.centrec.com/assets/profitability.pdf

Doğan, Z., Arslan, S., & Köksal, A. (2013). Historical development of agricultural accounting and difficulties encountered in the implementation of agricultural accounting. International Journal of Food and Agricultural Economics, 2(1), 107–116.

Evans, M. E., Houston, R. W., Peters, M. F., & Pratt, J. H. (2015). Reporting regulatory environments and earnings management: U.S. and non-U.S. firms using U.S. GAAP or IFRS. The Accounting Review, 90(5), 1969–1994. doi:10.2308/accr-51008

Farm Financial Standards Council. (2011). Financial guidelines for agricultural producers. Retrieved from http://msue.anr.msu.edu/uploads/files/firm/Analysis_and_Benchmarking/FFSC_Financial_Guidelines_2011.pdf

Figurek, A. (2015). The importance of recording data in the agricultural sector for decision-making. Oblik I Finansi, 67, 44–50.

Fischer, M., & Marsh, T. (2013). Biological assets: Financial recognition and reporting using US and international accounting guidance. Journal of Accounting and Finance, 13(2), 57–74.

Gillespie, J., & Mishra, A. (2011). Off-farm employment and reasons for entering farming as determinants of production enterprise selection in US agriculture. Australian Journal of Agricultural and Resource Economics, 55(3), 411–428. doi:10.1111/j.1467-8489.2011.00542.x

Ibendahl, G., Isaacs, S., & Trimble, R. (2002). Financial information base of participants in FSA borrower training. Journal of Extension, 40(5), Article 5RIB4. Available at: https://www.joe.org/joe/2002october/rb4.php

Internal Revenue Service. (2017). Accounting methods. Retrieved from https://www.irs.gov/publications/p334/ch02.html

International Accounting Standard. (2017). IAS 41—Agriculture. Retrieved from http://www.pkf.com/media/10033171/ias-41-agriculture-summary.pdf

Kay, R. D., Edwards, W. M., & Duffy, P. A. (2015). Farm management (8th ed.). New York, NY: McGraw-Hill, Inc.

Kurniawan, R., Mulawarman, A. D., & Kamayanti, A. (2014). Biological assets valuation reconstruction: A critical study of IAS 41 on agricultural accounting in Indonesian farmers. Procedia-Social and Behavioral Sciences, 164, 68–75. doi:10.1016/j.sbspro.2014.11.052

Marsh, T., & Fischer, M. (2013). Accounting for agricultural products: US versus IFRS GAAP. Journal of Business & Economics Research, 11(2), 79. https://doi.org/10.19030/jber.v11i2.7620

Miller, A., Barnard, F. L., Brown, N., Duckworth, B., Wheeling, B., & Wittmann, R. L. D. (2010). Farm enterprise analysis: Has it lost its usefulness? Journal of the American Society for Farm Managers and Rural Appraisers, 73(1), 199–206.

Ricketts, C., & Ricketts, K. (2009). Agribusiness: Fundamentals and applications (2nd ed.). Boston, MA: Cengage Learning.

Smetanka, R. (2012). GAAP or non-GAAP? Financial Executive, 28(9), 13–14.

U.S. Department of Agriculture. (2013). Small farms digest. Food Safety for Small Farmers, 16, 1–23.

U.S. Department of Agriculture. (2017). Farmer education. Retrieved from https://nifa.usda.gov/topic/farmer-education

Utegi, M., & Utegi, E. N. (2014). The importance of farm records and accounting in agricultural production. Katsina-Ala Multidisciplinary Journal, 2(1), ISSN: 2141-0992.

Vazakidis, A., Stergios, A., & Laskaridou, E. (2010). The importance of information through accounting practice in agricultural sector-European data network. Journal of Social Sciences, 6(2), 221–228.

Village Volunteers. (2011). Single entry bookkeeping. Retrieved from https://www.villagevolunteers.org/wp-content/uploads/2011/06/Basic-Bookkeeping.pdf

Wheeling, B. (2008). Introduction to agricultural accounting (1st ed.). Clifton Park, NY: Delmar Cengage Learning.