October 2018

|

October 2018 // Volume 56 // Number 6 // Ideas at Work // v56-6iw8

Youths Learn Responsible Use of Credit Cards

Abstract

The need for youth credit card education is clear given the many statistics indicating increasing credit card debt and an overall scarcity of credit card education targeting youths. The Teen$ Credit Card simulation program offers youths an opportunity to experience "owning" a credit card, using it, and realizing the consequences of carrying a high balance from month to month. Participants have a chance to discover the benefits and detriments of using a credit card in a safe environment before potentially making mistakes in real life. University of Idaho Extension educators have presented this program to over 550 youths in a variety of settings, with evaluation results indicating self-assessed increases in knowledge and planned positive behavior changes.

Background

The Federal Reserve has reported that Americans owe over $1 trillion in credit card debt (Board of Governors of the Federal Reserve System, 2017). In particular, college students aged 18 to 24 have an average credit card balance of $906 (Sallie Mae, 2016). Many youths struggle to understand concepts such as differences between credit cards and debit cards, and financial education can improve knowledge on such subjects and lead to positive financial decisions (Osteen, Muske, & Jones, 2007). Financial education for youths should be relevant and ensure effective motivation and should be offered at an early age (McCormick, 2009). In Idaho, educational standards include those related to credit and debt but do not directly address the use of credit cards (State Department of Education, 2016). This circumstance leaves many young people learning about credit cards though trial and error, not having the experience or education to understand the consequences of carrying a high credit card balance (Hayhoe, Leach, Allen, & Edwards, 2005). The 4-H youth development program reaches millions of youths nationwide with research-based educational experiences (National 4-H Council, 2018). In Idaho, Extension educators capitalize on the experiential nature of the 4-H youth development program to teach youths personal finance concepts in an innovative way, thereby helping them avoid the financial pitfalls afflicting many Americans today.

Program Description

Intended to help youths better understand personal finance and the consequences of using credit cards, the Teen$ Credit Card program allows youths to make mistakes and learn from them in a safe environment. To reach youths of all backgrounds, we have presented the program with several community partners and offered it in many nontraditional settings, including in church programs, school assemblies, and workshops. We also have taught the program at the Southwest Idaho Juvenile Detention Center, a site that requires ongoing program delivery because of the revolving nature of the audience. Youths at the detention center are at a higher risk of not completing high school, and personal finance typically is not taught to Idaho students until the senior year of high school. Personal finance education is critical to helping all teens understand that responsible decisions made today may affect their credit scores and, in turn, their future standards of living.

The Teen$ Credit Card program is a part of the Northwest Youth Financial Education program, a set of financial activities intended to help youths learn about personal finance and the importance of a good credit score. The Teen$ Credit Card program is designed for teens to gain experience in making financial decisions with credit cards. Youths learn how to distinguish between wants and needs, how to make wise spending decisions, and how to use credit cards responsibly. The program clarifies how interest and fees are charged and demonstrates that paying only the minimum balance on a card can negatively affect a person's financial well-being for several years. A hands-on experience, the program simulates the effects of using credit cards in a real-life scenario.

Specifically, teens participate in a hands-on credit card exercise whereby they each receive a simulated credit card with a credit limit of $1,000 or $2,000. They use their credit cards to make purchases at a virtual mall. After they finish shopping, they learn the true costs of using credit by discovering how much interest they owe and how long it will take them to pay off their credit card balances if they pay only the monthly minimum.

Methods and Impacts

From March 2016 to April 2017, educators conducted nine Teen$ Credit Card program workshops, reaching 561 teens. They presented workshop sessions in a number of settings, including in classrooms, at a school assembly, and at community events. They used retrospective pretest-and-posttest evaluation methods to measure both self-assessed change in knowledge and planned change in behavior of 163 program participants. Different assessment methods were used to measure outcomes of some workshops to meet grant requirements.

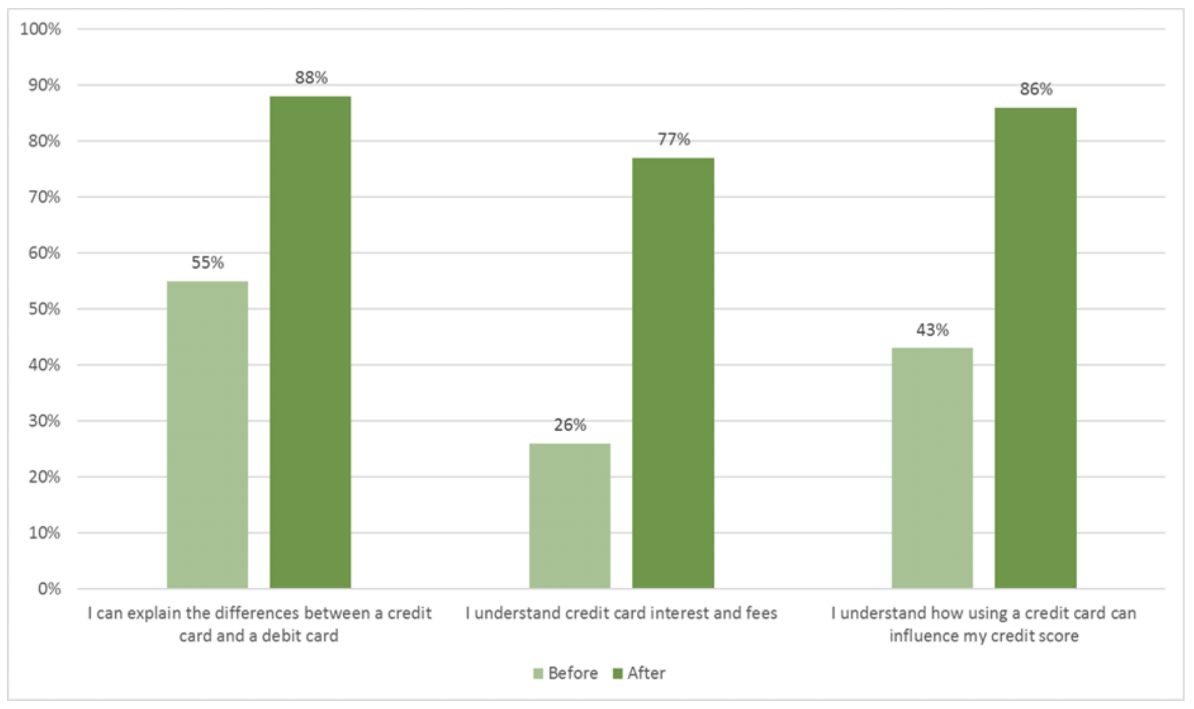

Findings of the self-assessment indicated changes in participants' understanding of the differences between a credit card and a debit card, credit card interest and fees, and the influence of using a credit card on one's credit score. Data are shown in Figure 1.

Figure 1.

Self-Assessed Changes in Participant Knowledge as a Result of Teen$ Credit Card Program (n = 163)

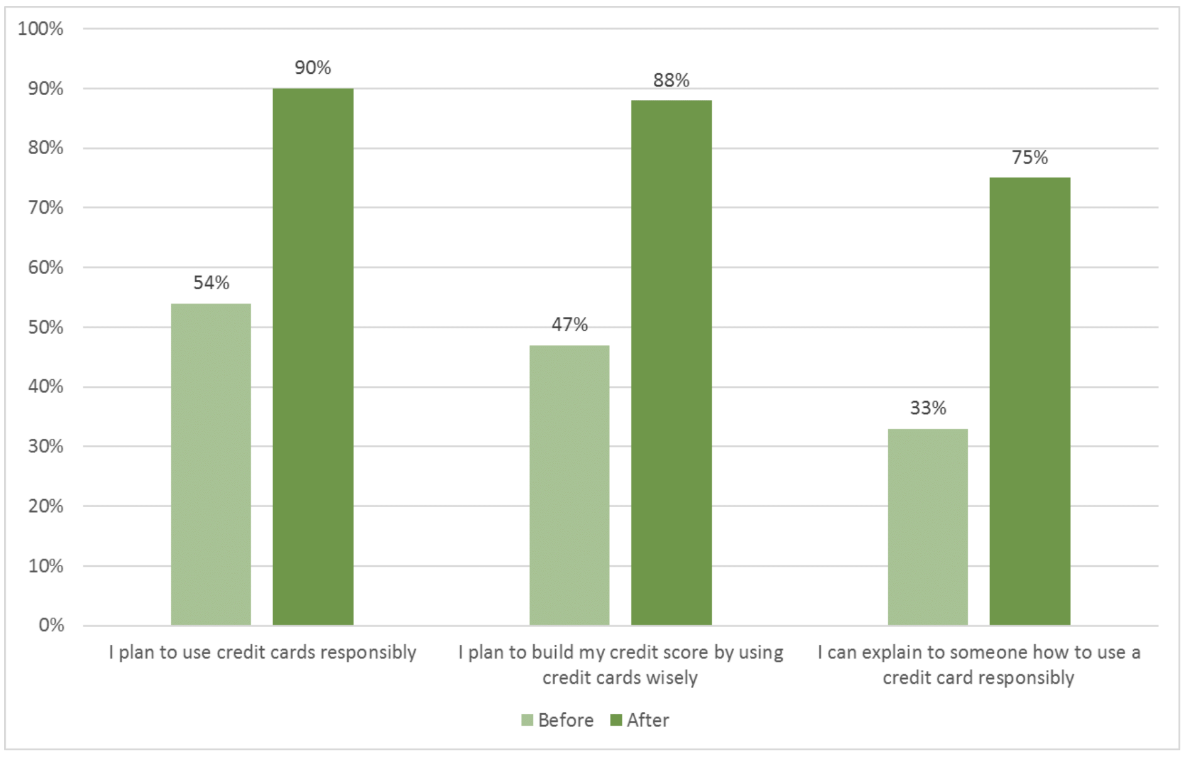

Findings also indicated that participants planned to make positive behavior changes in the areas of using credit cards responsibly and building a good credit score. Moreover, participants indicated being able to explain to others how to use a credit card wisely. Data are shown in Figure 2.

Figure 2.

Changes in Participants' Planned Behavior/Capability as a Result of Teen$ Credit Card Program (n = 163)

The evaluation also included the open-ended question "What changes do you plan to make because of this workshop?" Two of the responses were "I know now how to use a credit card to build good credit and plan on being able to do that in the future" and "Watch the way I use my credit card and watch the things I spend it on but always pay it off in full." Overall, results of the self-assessment indicated that participants were better prepared to use a credit card wisely.

Further Implementation

Delivery of the Teen$ Credit Card program will continue into the foreseeable future. A team of Extension professionals and volunteers currently deliver the program, and additional Extension professionals and volunteers are learning to present the program independently. By building the base of personnel capable of delivering the program, we further assure the sustainability of the program. The content of the program, lesson plan, and materials are easy to use, and delivering the program requires minimal preparation. To increase impact by illustrating differences in credit card offers and the need to "shop around" for the right credit card, we have added examples of real credit card offer disclosures to the program materials. All program materials are available on the University of Idaho 4-H Youth Development website (http://www.uidaho.edu/extension/4h/programs/nw-youth-financial-ed/programs/teens-credit-card) for Extension professionals to access and download.

The Teen$ Credit Card program may be used as a stand-alone program or as part of a bigger educational event. The versatility of the program allows it to be used in a number of settings, and it can be used successfully with groups of five to 200 teens.

References

Board of Governors of the Federal Reserve System. (2017). Total revolving credit owned and securitized, outstanding [REVOLSL]. Retrieved from https://fred.stlouisfed.org/series/REVOLSL

Hayhoe, C. R., Leach, L., Allen, M. W., & Edwards, R. (2005). Credit cards held by college students. Financial Counseling and Planning, 16(1), 1–10.

McCormick, M. (2009). The effectiveness of youth financial education: A review of the literature. Journal of Financial Counseling and Planning, 20(1), 70–83.

National 4-H Council. (2018). About 4-H. Retrieved from https://4-h.org/about/what-is-4-h/

Osteen, S., Muske, G., & Jones, J. (2007). Financial management education: Its role in changing behavior. Journal of Extension, 45(3), Article 3RIB2. Available at: https://www.joe.org/joe/2007june/rb2.php

Sallie Mae. (2016). Majoring in money: How American college students manage their finances. Retrieved from https://salliemae.newshq.businesswire.com/files/doc_library/file/SallieMae_MajoringinMoney_2016.pdf

State Department of Education. (2016). Idaho content standards: Social studies. Retrieved from http://www.sde.idaho.gov/academic/shared/social-studies/ICS-Social-Studies.pdf