October 2017

|

October 2017 // Volume 55 // Number 5 // Feature // v55-5a6

Reminding Individuals to Check Their Free Credit Reports: A Case for Using Low-Touch Campaigns to Promote Positive Behaviors

Abstract

This article describes University of Wisconsin–Extension's Check Your Free Credit Report Campaign. The program encourages adults to check their free credit reports through use of a memorable rule of thumb. The primary mechanisms of the program are a set of three email reminders each year and a campaign website. Data on program participation, engagement, and outcomes suggest that this program can complement higher touch financial education activities. Moreover, the format could be used to address other financial behaviors or extended to domains beyond consumer finance.

Introduction

This article describes a low-touch campaign that reminds adults to check their free credit reports, illustrating a format that may be useful for promoting other important but easy-to-forget activities. Extension educators often deliver financial education through more intensive, high-touch modes, such as workshops or one-on-one counseling or coaching (e.g., Collins, Olive, & O'Rourke, 2013; Petersen, Heins, & Katras, 2013). These higher touch approaches are foundational for developing financial capability, but lower touch approaches may be useful for complementing existing activities and reaching a broader audience (Drexler, Fischer, & Schoar, 2014).

Credit records affect individuals in critical ways, including whether they qualify for loans and how much they pay for credit and insurance. In addition, many employers check credit reports when making hiring decisions, and landlords often check them when considering potential tenants (Federal Deposit Insurance Corporation, 2016). The credit reporting system puts the responsibility for identifying and correcting errors in reports on individuals. Beyond checking for errors, reviewing their credit reports can help individuals detect identity theft and identify ways to improve their credit (Birkenmaier & Curley, 2009). Thus, it is important for individuals to review their credit reports regularly.

By law, Americans can check their credit reports from each of the three major reporting bureaus—Equifax, Experian, and TransUnion—for free once every year. Identity theft and other circumstances may increase the number of free reports available to an individual (Federal Trade Commission, 2013). A website (https://www.AnnualCreditReport.com) and its associated telephone number and mailing address are the only official sources for these free reports, which contain the same information as reports that individuals may pay for but that do not include a credit score.

Data on the percentage of Americans who check their credit reports each year is difficult to come by, as many researchers combine credit scores and reports into a single survey question. Nonetheless, national surveys have indicated that only around 30% to 40% of adults obtain credit reports each year (e.g., Consumer Federation of America, 2016; FINRA Investor Education Foundation, 2012), as opposed to credit scores, which are increasingly available for free from creditors or companies such as Credit Karma, leading more consumers to access them (O'Neill & Xiao, 2014). A problem with this situation is that credit scores alone provide little to no education or actionable information. Credit reports, which are more difficult to obtain than scores, contain detailed information that individuals can verify and use to identify steps toward improving their credit histories.

Failing to check credit reports can have real consequences for consumers' financial lives as errors in credit reporting can affect their financial options. Errors do exist in a small yet significant percentage of credit reports. In a study by the Federal Trade Commission (2012), 21% of participants had at least one error in at least one credit report that was ultimately corrected by the reporting agency. More than half of those disputes affected participants' credit scores; 5% of study participants saw changes in their credit scores as a result of resolving an error that likely would affect how much they would pay for an auto loan. These kinds of errors affect millions of Americans, and it is impossible to identify and correct errors without reviewing an actual report. Thus, regularly reviewing credit reports is an important financial activity.

Here, we describe University of Wisconsin–Extension's Check Your Free Credit Report Campaign and report on data collection techniques we used during the campaign and the resulting findings. We conclude with a discussion of those results and implications for the delivery of Extension programming.

Program Description

University of Wisconsin–Extension started the Check Your Free Credit Report Campaign in January 2013. The campaign, which is ongoing, consists of several components, including email reminders, a website, social media engagement, and county-level efforts. Because there are three credit reporting bureaus, each of which is required to provide consumers one free credit report per year, outreach efforts are organized around three dates each year—February 2, June 6, and October 10; these easy-to-remember dates, 2/2, 6/6, and 10/10, are touchstones of the program. The campaign encourages individuals to check one credit report on each of these dates as a way to monitor their credit. Centering the campaign around the same set of dates each year is intended to organize educators' efforts and focus the public's attention over time.

The activities associated with the campaign are designed around low-touch mechanisms for encouraging people to take actions that promote financial security and, especially, to check their credit reports. State-level staff maintain the website and disseminate materials to county educators, who share resources and ideas for promoting the campaign locally. Beyond drafting news releases and developing new county-level outreach materials, county educators do not need to perform any significant ongoing maintenance associated with the campaign.

Email Reminders

Increasing awareness and monitoring of credit records may help individuals better manage their credit (Lyons, Rachlis, & Scherpf, 2007). Reminders may help bring financial information back to the "top of the mind" and ultimately affect behavior (Karlan, McConnell, Mullainathan, & Zinman, 2016). The core of the campaign is a set of email reminders designed to do just that by bringing the topic of credit and credit reports to participants' email in-boxes at regular intervals.

Participants, who sign up on the campaign website, receive email reminders on the three target dates (February 2, June 6, and October 10) each year. We use these fixed dates as focus points for marketing efforts; the systems used to support the campaign do not allow for individualized reminders based on the exact date individuals sign up or report last checking a credit report. Email reminders were selected over text messages primarily due to concerns about accessibility (older audiences are less likely to use text messages) and cost. Although text messaging has become more prevalent since the campaign started in 2013, the campaign continues to rely on one reminder system, emails, to keep administrative burdens low.

The first reminder was emailed February 2, 2013. Figure 1 shows the email reminder text. The email reminders direct recipients to the official website for free reports, AnnualCreditReport.com (https://www.annualcreditreport.com), and to the campaign website. To date, the highest bounce rate for a round of email reminders is only 3%, indicating that the emails are reaching the target audience.

Figure 1.

Email Reminder Text

Website

To remain relevant on the Internet, Cooperative Extension programs must provide unbiased content based on stakeholders' needs (Rader, 2011). A dedicated campaign website (http://fyi.uwex.edu/creditreport) highlights why it is important to check credit reports regularly. At the site, visitors can learn about the process of requesting and reading their reports and what to do if they find errors. Recognizing that credit reports may be intimidating, especially for people reviewing them for the first time, the site also provides resources to help make the process more straightforward and links to credible resources, including referrals to county Extension educators for individualized assistance.

News Releases

Print and radio releases are prepared around each target date. Each release focuses on a different topic around credit reports—for instance, the difference between a credit report and a credit score—and highlights the email reminders and website. County educators are encouraged to customize the news releases for their local communities.

Social Media Outreach

County educators and project partners promote the campaign through social media on and around the three dates, working from a provided social media packet that includes suggested Tweets and Facebook posts. In addition, we experimented with sidebar advertisements in Facebook, the earliest effort of its kind for Wisconsin Cooperative Extension Family Living programs. The advertisement read "Finances need a check-up? University of Wisconsin–Extension can help you check your free credit report!" The advertisement, which cost $50, was displayed for 3 days around February 2, 2013. The only targeting for the ad was to Wisconsin residents. The ad resulted in 75 clicks through to the campaign website—representing a cost of 66 cents per click; because the sign-up form does not capture referral source, we cannot say how many reminder sign-ups the ad generated.

County-Level Strategies

County Extension educators have engaged in a variety of efforts to encourage individuals to sign up for the email reminders, including airing local radio spots, setting up informational displays in public buildings, and displaying posters. A work group of county educators and specialists collaborate to develop and disseminate strategies for promoting the campaign. Educators often link the campaign to other financial education activities. A recent study focused on the challenges of increasing positive financial behaviors suggested that there is a critical window of opportunity after an engagement where behavior change may be cemented through follow-up contact (Fernandes, Lynch, & Netemeyer, 2014). To maximize this window of opportunity, county-level educators frequently encourage participants to sign up for reminders during workshops related to credit management.

Results

The findings we present here are from data collected during the campaign. The data on the program impacts are from three sources: reminder sign-ups (data collected January 2013–February 2016), email analytics (February 2015–February 2016), and an online survey of participants (October 2015). Each data set was cleaned, a process that largely focused on removing duplicate email addresses, and the data sets were linked using email address as the unique identifier.

Email Reminder Sign-Up Rates

The email sign-up form initially included only a field for the individual's email address. A question added in May 2013 addressed the individual's location (county for those in Wisconsin, state for those outside the state), and a question added in January 2015 addressed how many times the participant had ordered a credit report in the preceding year.

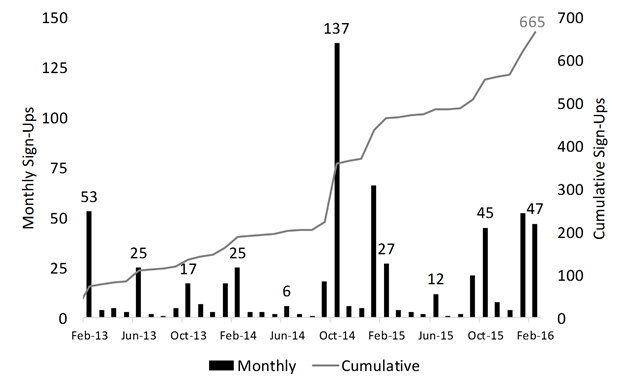

A total of 665 individuals signed up for email reminders through February 2016. Figure 2 displays both monthly and cumulative reminder sign-ups. The cyclical nature of the campaign is visible in the chart, with spikes in February, June, and October of each year. The more general ebb and flow of sign-ups reflects the organization and momentum behind the campaign. For example, in the more recent periods, news releases were provided to county educators earlier, giving them longer to promote the campaign. The average number of sign-ups per month was 17 across all months and 39 in the campaign months. The minimum number of sign-ups in a month was one, and the maximum 137. Figure 2 documents an overall steady increase in sign-ups over time, with a slight acceleration apparent in the more recent half of the study period. The steady increase in sign-ups suggests that the campaign has not exhausted its potential for growth.

Figure 2.

Email Reminder Sign-Ups, February 2013–February 2016

Overall, 93% of sign-ups came from Wisconsin residents; individuals in 21 other states made up the remaining 7%. Wisconsin sign-ups were dispersed across the state, with participants from 62 of the state's 72 counties; 12 counties had 10 or more sign-ups. Variations across counties likely reflect population differences as well as differences in local promotional efforts. Although these numbers are by no means large relative to the overall population of the state, the campaign stands as one of the University of Wisconsin–Extension's largest adult financial education initiatives. Because individuals who sign up for reminders continue to receive the emails into the future, the intervention's communications with participants are much greater than the number of sign-ups. For example, an individual who signed up for reminders in January 2013 received 10 reminders through February 2016.

Email Reminder Analytics

A change to a new system in January 2015 made available data on email bounces and opens, along with clicks on the links to AnnualCreditReport.com and the campaign's website. These data, which were available for four reminder cycles in the study period, offer insight into the effectiveness of the reminder emails. These analytics were available for 456 email addresses in February 2015, increasing to 618 addresses for the February 2016 reminder email. The number of emails is less than the total number of campaign sign-ups due to attrition (e.g., unsubscribing) over time.

Table 1 shows the total number of successful (nonbounced) emails at each contact point between February 2015 and February 2016, the percentages of recipients who opened the emails, and the percentages of recipients who clicked the links. Email opens decreased slightly, from 56% in February 2015 to 50% for the most recent email cycle. Combining clicks to either website, between 14% and 19% of recipients clicked at least one link in each email. The vast majority of these clicks were to AnnualCreditReport.com. The decrease in email opens and clicks over time suggests a slight decline in engagement, something we are monitoring.

| Email date | Successful emails | Opened email | Clicked email links | |

| AnnualCreditReport.com | Campaign website | |||

| February 2, 2015 | 456 | 56% | 18% | 5% |

| June 6, 2015 | 485 | 52% | 15% | 2% |

| October 10, 2015 | 529 | 52% | 16% | 3% |

| February 2, 2016 | 618 | 50% | 13% | 2% |

| Note. Source: Campaign database maintained on MailChimp.com. Data as of March 8, 2016. Excludes bounced emails. | ||||

To explore email opens and clicks over time in more depth, we identified 456 individuals who signed up for reminders before February 2015. We tracked these individuals over time to see whether they opened or clicked links in the four reminders through February 2016. Among these individuals, 19% opened none of the four emails, 41% opened one or two of the emails, and 40% opened three or four of them. Turning to clicks, 37% of the 456 individuals clicked a link in at least one of the four subsequent emails, and 5% clicked a link in three or four of the emails.

Follow-Up Survey

Although participants' engagement with emails, in the form of opens and clicks, is an important signal of the campaign's success, the ultimate goal is to increase the frequency with which individuals check their credit reports. A follow-up survey, administered in October 2015, sheds light on whether the campaign accomplishes this goal; the University of Wisconsin–Extension Institutional Review Board approved the survey (IRB# 2016-83). The survey, which was developed by the campaign's work group and emailed to participants who had signed up for reminders, was designed to measure whether the campaign resulted in an increase in participants requesting credit reports, to document what people who requested their credit reports did with them, and to assess respondents' credit knowledge. Out of 529 emailed surveys, 138 individuals completed the follow-up survey, for a response rate of 26%. No incentives were provided.

An analysis of the sign-up data showed that survey respondents had signed up for the campaign an average of 23 days earlier than nonrespondents, a small difference given that sign-ups spanned 1,048 days. At sign-up, respondents and nonrespondents had checked their credit reports in the past year at about the same frequency; the difference between the two groups was not statistically significantly different at the 10% level. More detailed analysis of differences between survey respondents and nonrespondents is not possible because the sign-up form allows for only limited information.

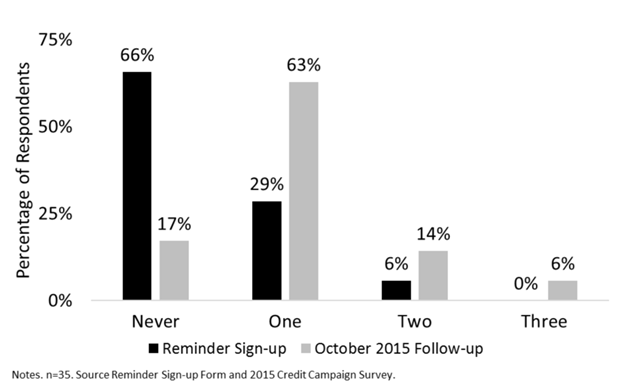

Thirty-five survey responses could be matched to data from the sign-up form regarding how many times the individual had ordered credit reports in the preceding year. The matched sample size was so small because the question was not added to the form until January 2015. Figure 3 compares the responses at sign-up and on the survey. At sign-up, two thirds of the 35 matched respondents reported having never requested a credit report in the preceding year; only 17% reported never having requested a report.

Figure 3.

Number of Times Participants Had Requested Credit Reports in the Preceding Year

At sign-up, the 35 respondents had checked their credit reports an average of 0.4 times in the past year, a figure that more than doubled to 1.1 on the follow-up survey. This increase, which is statistically significant at the 1% level, potentially underrepresents the impact of the campaign in changing participants' behavior because individuals who signed up later had received only one or two reminders when the survey was sent—an individual who signed up in September 2015 would have received only one email reminder before receiving the survey. More detailed analysis of the effect of repeated reminders over time is not possible given the small sample size. Nonetheless, the documented increases suggest that the campaign does produce its intended outcome of more frequent checking of credit reports.

The survey asked individuals who had requested credit reports how they had made their most recent request. The overwhelming majority, 94%, had done so online, with 5% submitting a mailed form and 1% calling the toll-free number (n = 127). Just 5% of respondents reported having trouble accessing their reports. Respondents also reported on the results of reviewing their most recent reports: 83% of respondents reported finding no errors, 7% contacted a creditor or credit bureau to fix an error, 5% identified at least one way to improve their credit, and 2% obtained help in reviewing their reports through their local Extension office (n = 134).

The survey asked all respondents to assess their levels of knowledge of credit and credit reporting on a 5-point scale, ranging from nothing to a lot (n = 137). On this scale,

- 40% of respondents reported knowing very little or nothing about how long information stays in a report;

- 17% reported knowing little or nothing about how information gets onto a report; and

- 14% reported knowing little or nothing about how information in a credit report affects their credit score.

These findings will be used to focus educational efforts, media messaging, and website content.

Conclusion

The program described here involves use of a low-touch approach to influence consumer behavior. The sign-up data and email analytics provide automated, real-time data that are valuable for tracking engagement over time; the survey provides more detailed insight into changes in participants' behavior. Taken together, the data indicate a steady increase in sign-ups over time and are suggestive of an increase in the frequency with which participants check their credit reports.

Lower-touch financial education activities allow educators to expand their impact and increase public awareness with minimal additional resources. The challenge rests in balancing low-touch strategies with programs that support those learners who may be interested in more intensive education. Going forward, the program will continue to experiment with ways to increase engagement, most immediately by testing different messaging in the reminders.

The basic components of the campaign described here could be extended to other domains, financial or otherwise, to promote activities that are important but easy to forget. For instance, a reminder program could be used to encourage individuals to check their Social Security statements each year. Reminders could also be used to promote beneficial health behaviors, such as regular checkups. Many key design features, including the framing and timing of the reminders, merit further research. Nonetheless, our campaign demonstrates that a straightforward set of reminders delivered at regular intervals holds potential to encourage positive behaviors that are often overlooked.

References

Birkenmaier, J., & Curley, J. (2009). Financial credit: Social work's role in empowering low-income families. Journal of Community Practice, 17(3), 251–268.

Collins, J. M., Olive, P., & O'Rourke, C. (2013). Financial coaching's potential for enhancing family financial security. Journal of Extension, 51(1), Article 1FEA8. Available at: https://www.joe.org/joe/2013february/a8.php

Consumer Federation of America. (2016). Credit score knowledge 2016—Summary of survey results. Retrieved from http://consumerfed.org/reports/press-teleconference-summary-credit-score-knowledge-2016

Drexler, A., Fischer, G., & Schoar, A. (2014). Keeping it simple: Financial literacy and rules of thumb. American Economic Journal: Applied Economics, 6(2), 1–31.

Federal Deposit Insurance Corporation. (2016). Credit reports basics. Retrieved from https://www.fdic.gov/consumers/assistance/protection/creditreport.html

Federal Trade Commission. (2012). Report to Congress under Section 319 of the Fair and Accurate Credit Transactions Act of 2003. Retrieved from https://www.ftc.gov/sites/default/files/documents/reports/section-319-fair-and-accurate-credit-transactions-act-2003-fifth-interim-federal-trade-commission/130211factareport.pdf

Federal Trade Commission. (2013). Free credit reports. Retrieved from https://www.consumer.ftc.gov/articles/0155-free-credit-reports

Fernandes, D., Lynch, J. G. Jr., & Netemeyer, R. G. (2014). Financial literacy, financial education, and downstream financial behaviors. Management Science, 60(8), 1861–1883.

FINRA Investor Education Foundation. (2012). Summary of selected findings. Results from the FINRA Investor Education Foundation US Financial Capability Study. Retrieved from http://www.usfinancialcapability.org/downloads/tables/U.S._2012.pdf

Karlan, D., McConnell, M., Mullainathan, S., & Zinman, J. (2016). Getting to the top of mind: How reminders increase saving. Management Science. Advance online publication. doi:10.1287/mnsc.2015.2296

Lyons, A. C., Rachlis, M., & Scherpf, E. (2007). What's in a score? Differences in consumers' credit knowledge using OLS and quantile regressions. Journal of Consumer Affairs, 41(2), 223–249.

O'Neill, B., & Xiao, J. J. (2014). Post-recession, post legislation credit use: Insights from an online survey. Journal of Personal Finance, 13(1), 65–76.

Petersen, C. M., Heins, R. K., & Katras, M. J. (2013). Dollars Works 2: The evolution of a financial literacy program. Journal of Extension, 51(2), Article 2TOT8. Available at: https://www.joe.org/joe/2013april/tt8.php

Rader, H. B. (2011). Extension is unpopular—on the Internet. Journal of Extension, 49(6), Article 6COM1. Available at: https://www.joe.org/joe/2011december/comm1.php