February 2013

|

February 2013 // Volume 51 // Number 1 // Feature // v51-1a8

Financial Coaching's Potential for Enhancing Family Financial Security

Abstract

Financial coaching is an emerging complement to financial education and counseling. As defined in this article, financial coaching is a process whereby participants set goals, commit to taking certain actions by specific dates, and are then held accountable by the coach. In this way, financial coaching is designed to help participants bridge the all-too-common gap between knowledge and intentions on the one hand and lasting behavior change on the other. After introducing the financial coaching process, this article highlights recent Extension coaching initiatives and overviews findings from survey data from coaching trainings and a coaching partnership with Head Start.

Introduction

Extension's longstanding strength of delivering financial management programs has taken on heightened importance in light of the Great Recession's effects on family financial security. Extension activities in this area have traditionally involved financial education and counseling. Past studies on these approaches have generally documented improvements in participants' knowledge and behavior (O'Neill, 2006; O'Neill, Xiao, Bristow, Brennan, & Kerbel, 2000; Osteen, Muske, & Jones, 2007).

Financial coaching is an emerging complement to these core approaches. As defined in this article, financial coaching is an ongoing process that involves setting goals, establishing a concrete plan of action, monitoring one's progress, and, ideally, forming new positive financial habits. In this way, financial coaching has the potential to assist individuals who are contemplating behavior change in overcoming all-too-human barriers to lasting change, including procrastination and lapses in self-control, in order to reach their self-determined goals.

In practice, the term "financial coaching" has been used to refer to numerous types of interventions, many of which diverge significantly from the approach described in this article. A quick Internet search yields a range of programs labeled "financial coaching," "money coaching," "debt coaching," and any number of related terms. In a similar vein, Grant and Cavanagh (2011) note that "anyone can call themselves a coach, and the practice of coaching is unregulated" (p. 295). In light of this ambiguity, one of this article's goals is to delineate financial coaching as a distinct intervention that draws upon coaching psychology and adult learning theory. Financial coaching as defined in this article is not simply a rebranding of existing financial capability-building approaches.

In recent years, Extension family living educators with the University of Wisconsin-Extension (UW-Extension) have engaged in several initiatives to promote financial coaching in Wisconsin and beyond. These initiatives include training new financial coaches, creating programs that match trained financial coaches to community members interested in working with a coach, and directly coaching individuals. One leading example of UW-Extension's financial coaching initiatives is the Money $mart in Head Start program, which offers financial coaching to low-income parents of preschool children.

Throughout these initiatives, UW-Extension family living educators have devoted significant time and resources to gathering survey data, both from individuals who attended coaching trainings and from individuals who were coached. Using these data, this article highlights research findings from UW-Extension's financial coaching initiatives. The remainder of this article is broken into four sections. First, financial coaching is defined in greater detail. Second, the article highlights UW-Extension's efforts to expand the availability of financial coaching in Wisconsin. Third, the article presents research findings from recent UW-Extension financial coaching initiatives. The article concludes with closing thoughts on the promise of coaching and on some of the challenges for the field.

Overview of Financial Coaching

Individuals interested in working with a financial coach have often tried to change their behavior, only to fail to follow through on their intentions. Recognizing the challenges inherent in behavior change, financial coaches help participants form concrete action plans, hold participants accountable to their stated intentions, and offer support along the way. Financial coaching is intended to strengthen participants' willpower and ultimately help them develop new skills so they can take greater control of their personal finances.

Financial coaching draws upon the more general field of coaching. One leading researcher defines coaching as "a collaborative solution-focused, result-orientated and systematic process in which the coach facilitates the enhancement of life experience and goal attainment in the personal and/or professional life of normal, nonclinical clients" (Grant, 2003, p. 254). This definition highlights several core features of coaching. Throughout the coaching process, the participant and the coach are equals working together towards the participant's goals. A coach is a facilitator rather than an educator or advisor. In fact, one of the most common frustrations novice coaches experience stems from having to avoid telling participants what to do. Instead, coaches allow participants to define their own vision of success, which in turn eases the coach's burden of having to function as an expert on the participant's financial decisions.

Moreover, coaching is future-oriented and is focused on helping participants attain measurable goals. To a casual observer, coaching may appear unstructured and driven solely by the client, when in fact coaches are trained to engage in a systematic process of active listening and critical questioning. Most notably, the coaching framework is best suited for "non-clinical" populations, meaning individuals who possess sufficient internal resources to engage in the process of behavior change. As such, coaching is likely inappropriate for people dealing with acute crises. People in crisis can often benefit from more directed services such as financial counseling. In addition to the features highlighted in Grant's definition of coaching, financial coaching draws upon principles relevant to adult learning (e.g., self-direction) while emphasizing psychological mechanisms, including goal orientation and external support, that are particularly relevant to personal financial management.

Again, most participants are attracted to financial coaching because they have a goal in mind but need some help in attaining it. Participants enter financial coaching with goals that range from general to specific and from short-term to long-term. Oftentimes, participants enter coaching with vague notions about the steps they would like to take financially, such as "saving more money." In other cases, participants enter coaching with more concrete goals already in mind. For example, a participant may want to accumulate $500 in an emergency fund by the end of the year. In some instances, a participant's goals may be unrealistic given the individual's resources. The coach's first task is to work with clients on refining their goals.

Financial coaching assumes that participants have a sense, however vague, of how they want to improve their financial circumstances. Nevertheless, participants' financial aspirations may not be amenable to concrete, actionable steps. A participant may want to "fix my credit" or "save more money," but these goals are not defined in ways that lend themselves to specific actions within a given timeframe. Furthermore, all-too-human behavioral tendencies such as procrastination and distraction may prevent participants from achieving even the most well-defined goals. Recognizing these impediments to goal attainment, the financial coaching model helps participants develop action-oriented goals and overcome behavioral impediments to change. Coaches reserve judgment about the merits of an individual's goals and instead use the coaching framework to assist participants in clarifying and reaching their financial goals through an iterative process that may last 6 to 12 months or more. Throughout this process, the goal serves as both a motivational device and as a tool to focus the participant's attention on certain tasks and behaviors.

Coaches are trained in a range of techniques, including powerful questioning, to help participants refine their goals and develop realistic action plans. Critically, the coach documents what the participant says he or she will do and by when, and then follows up to hold the participant accountable to these commitments. The coach also helps the participant define and articulate the latter's competencies, resources, and desires. Coaches often work with participants to break down overarching goals into several smaller steps, with the participant committing to complete each step by a particular date. Suddenly, a vague goal that initially seemed elusive becomes more manageable, and the participant has a concrete, yet self-defined, plan of action. This approach to facilitating participants' goal attainment is broadly consistent with well-known models of behavior change, including the theory of planned behavior (Ajzen, 1991) and the transtheoretical model of behavior change (Prochaska, DiClemente, & Norcross, 1992).

Of course, having a well-defined goal by no means guarantees that the participant will make timely progress toward that goal. Even participants with well-defined goals may struggle to save small amounts of money, pay down debt, or pay bills on time to avoid late fees. Thus, financial coaches are also charged with holding participants accountable, providing encouragement, and praising their success.

To illustrate this process, one can think of a coaching participant who wants to establish a $500 rainy day fund by the end of the year. This individual may start by tracking his or her spending for 1 month to gain a better understanding of how much money he or she can realistically set aside. Throughout this 1-month period, the participant will likely face competing demands for his or her attention and resources. Ideally, having set a concrete plan of action and being held accountable by a third party help the participant stay the course. Once the month has passed, the coach checks in with the participant to see whether the individual succeeded in tracking his or her spending. If the participant successfully follows through, the coach and participant celebrate this achievement and agree on the participant's next set of goals and timelines. If the participant is unsuccessful, the coach and participant work together to refine the strategy for accomplishing the goal. This process may even involve reformulating the goal altogether.

In terms of the coaching timeline, the coach and participant typically meet in person for the first two to three sessions in order to establish trust and rapport. Additional sessions may occur in person, on the telephone, via email, or even through text messages. For some coaching participants, a single sentence via email or text may be enough to remind them of their goals and thereby encourage them to stick to their plan of action. Being held accountable to a third-party enhances self-control and also helps keep intended behaviors in the forefront of participants' minds. Multiple studies indicate that mechanisms that motivate and systematize disciplined financial behavior enhance individuals' ability to sustain behavioral changes (Hilgert, Hogarth, & Beverly, 2003; Robb & Woodyard, 2011; Shockey & Seiling, 2004).

Building the Capacity of Financial Coaching

Extension educators are skilled in providing financial counseling, financial education workshops, and financial trainings for community partners. Given the growing interest in transformational education and behavioral economics, financial coaching was seen as a promising complement to these core approaches. Recognizing the potential of financial coaching for assisting individuals in reaching their financial goals, in 2009 the UW-Extension began building the system's capacity to deliver coaching within Wisconsin communities.

Training Financial Coaches

Extension began its work in this area by developing a cohort of trained financial coaches. Because financial coaching is a relatively new field, training opportunities for financial coaches are limited. Recognizing this gap, two UW-Extension family living educators participated in an intensive financial coaching train-the-trainer program offered by the Central New Mexico Community College (CNM). CNM is a national leader in delivering coaching to its students and in training new coaches across the nation. To date, UW-Extension's coaching trainers have trained 93 individuals from across Wisconsin in financial coaching. This total includes 37 Extension family living educators from an estimated 25 Wisconsin counties. In addition to Extension educators, these one-day trainings have attracted housing counselors, human service professionals, and individuals from the financial services sector. Each session involves hands-on learning and peer coaching, as well as pre-reading and follow-up communications. UW-Extension and its partners have also developed a website that provides ongoing support and information to financial coaches, as well as a quarterly newsletter to keep in touch with coaches.

Delivering Financial Coaching

Many educators are using coaching techniques as part of ongoing education and counseling programs, but several initiatives specific to coaching have emerged. In one initiative, an Extension educator serves as a coordinator for community-based volunteers. The Extension educator recruits volunteers, trains them in financial coaching, and then helps match the volunteers with individuals interested in working with a financial coach. This program entails a structured 6-month meeting schedule that includes workshops and other opportunities for coaches and clients to interact. To date, more than 25 volunteer coaches have been trained, and 50 individuals have entered into financial coaching.

Extension educators have also worked directly as financial coaches. Most significantly, financial coaching was a component of a recent partnership between Head Start and UW-Extension. During the 2010-2011 school, Head Start programs in 16 Wisconsin counties participated in the Money $mart in Head Start (M$iHS) initiative. The M$iHS program offered a mixture of three financial capability-building interventions to Head Start families: financial coaching, monthly financial newsletters, and financial literacy workshops. Head Start staff members and UW-Extension family living educators collaborated to promote the M$iHS program and collect survey data. Extension family living educators delivered the program's financial capability-building services, including financial coaching, to Head Start parents. The M$iHS program represents a novel approach to integrating financial coaching into an existing public program in order to reach lower-income families.

Data Analysis

UW-Extension family living educators have collected data from their financial coaching trainings and from the M$iHS program. These data shed light on interest in financial coaching among prospective financial coaches and participants, as well as the potential benefits of UW-Extension's financial coaching initiatives to date.

UW-Extension Financial Coaching Trainings

All participants at UW-Extension's 1-day trainings were asked to complete a baseline survey. The survey asked respondents about their personal and professional backgrounds and about their views on various financial matters that could arise during financial coaching. Eighty-six of the 93 participants completed this survey, for a response rate of 92%.

The diversity of respondents' backgrounds suggests that financial coaching holds broad appeal. Less than one-half (44%) of respondents were Extension educators, about one-quarter (27%) were financial or housing counselors outside of Extension, and the remainder generally worked for other local or state public agencies. Respondents tended to have high educational attainment. Nearly all held a bachelor's degree, and 36% held a master's degree. Thirty-eight percent of respondents had worked in their field or profession for 3 years or less, 31% had done so for 4 to 12 years, and 32% had done so for 13 or more years.

The latter figure could prove particularly important to the growth and sustainability of coaching to the extent that individuals who have worked in their field or profession longer are more likely to have attained leadership positions within their organizations. Surveys that were administered at three of the five UW-Extension trainings (n=60) indicate that financial coaching was a new approach for three-quarters of respondents. This lack of familiarity suggests that financial coaching in the form described in this article is not widespread. Even respondents who were familiar with coaching tended to have had minimal prior exposure to this approach, based on their responses to an open-ended question.

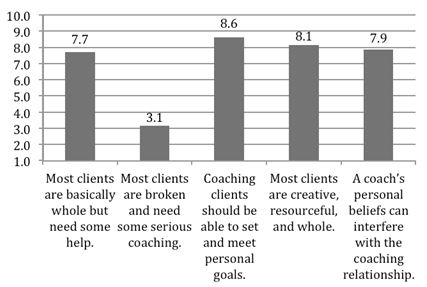

Participants were also asked to complete follow-up surveys 2 weeks after each training. A total of 42 participants responded to these surveys, for a response rate of 45%. Respondents had strong intentions to integrate financial coaching approaches into their work, and only five respondents (12%) to the follow-up survey indicated that they did not plan to use coaching skills in the next 6 months. In contrast, nearly 61% of respondents planned to use coaching with at least six clients over the next 6 months. Figure 1 shows that most trained coaches embraced the coaching approach. The figure displays the mean responses to a series of questions using 10-point scales, with 10 indicating strong agreement and 1 indicating strong disagreement. Overall, respondents viewed coaching participants as capable of setting and reaching their own goals. They also acknowledged the risk of imposing their own beliefs on participants and the undesirability of doing so.

Figure 1.

Coaching Training Follow-Up Survey Responses

(10=strongly agree, 1=strongly disagree)

Source: UW-Extension Coaching Training Follow-up Survey, n=42

Money Smart in Head Start

Throughout the 16 Wisconsin counties that took part in the 2010-2011 M$iHS program, parents of children enrolled in Head Start were asked to complete a survey in the fall of 2010. The surveys were administered during home visits, through the Head Start sites, and at special events. Just over 500 households responded to this survey, of about 1,500 households with children at the participating sites. The survey covered a range of topics, including whether respondents were interested in working with a financial coach to reach their goals.

Table 1 compares the survey responses of those who were interested in coaching versus those who were either not interested in or unsure about coaching. Overall, about one-third (36%) expressed interest in working with a financial coach. There were some stark differences between the two groups—respondents interested in coaching and those who were either uninterested or unsure. Importantly, parents who reported an interest in coaching were more likely to have a financial goal (verified in the survey by asking respondents to write down that goal). The groups were equally confident in achieving their goals, as this is the only variable in Table 1 without a statistically significant difference. Mean confidence in achieving goals was low for both groups. Parents interested in coaching also appear to face more challenges. They reported more difficulty in paying their loans or debts and low confidence in their ability to save and budget. Respondents interested in coaching also reported greater financial stress than parents who were not interested in or unsure about working with a coach. Overall, these results are consistent with the concept that individuals interested in coaching have financial goals, but that they have struggled in the past to change their financial behaviors.

| Interested in Coaching | Not Interested in or Unsure About Coaching | |

| Number of respondents / households | N=178 | N=323 |

| Have at least one financial goal? | 76% | 65% |

| Confidence in reaching this goal within the next year (5-point scale: 1=not at all confident, 5=certain) | 2.6 (ns) | 2.5 (ns) |

| Find it difficult to pay any of your loans or debts? | 72% | 53% |

| Confidence in saving for the future? (10-point scale: 1=low confidence, 10=high confidence) | 3.9 | 4.6 |

| Confidence in budgeting? (10-point scale: 1=low confidence, 10=high confidence) | 4.7 | 5.9 |

| Currently, how much stress do you feel about your financial situation? (10-point scale: 1=no stress, 10=overwhelming stress) | 7.6 | 6.4 |

|

Source: UW-Extension Money $mart in Head Start Fall 2010 Survey, n=501. All comparisons are statistically significant at the 99% level except the one marked as (ns) |

||

Conclusion

The financial coaching model described in this article remains a relatively new approach to building individuals' financial capability, especially when compared to the long-established financial education and counseling fields. Financial coaching is a potentially powerful complement to these widely established approaches. Because financial coaching focuses so intently on behavior change, it holds great promise for working with families to improve their financial security. At its core, financial coaching is designed to turn knowledge and intentions into action by enhancing individuals' self-control, focusing their attention, and holding them accountable. Financial coaching can be used to extend education and counseling in new and important ways.

Starting a coaching program, however, comes with its own set of challenges. Few training programs or manuals exist, though more training resources are becoming available. Becoming a coach involves developing particular skills and approaches to working with participants, rather than learning to adhere to a set curriculum. Learning to be a coach requires hands-on practice with supervision, which can prove resource intensive. Coaching clients also appear to have a wide range of needs, and, by definition, coaching will reach fewer participants than group-based strategies. Because lasting behavior change often proves so challenging, financial coaching may play an important role in future financial capability-building strategies.

Acknowledgments

Support for this project was provided by the Annie E. Casey Foundation. The authors are grateful for research assistance from Melissa Berger and program support from Wisconsin Cooperative Extension Family Living Programs and county-based educators.

References

Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179-2011.

Grant, A. M. (2003). The impact of life coaching on goal attainment, metacognition and mental health. Social Behavior & Personality: An International Journal, 31(3), 253-263.

Grant, A. M., & Cavanagh, M. J. (2011). Coaching and positive psychology. In T. B. Kashdan, K. M. Sheldon & M. F. Steger (Eds.), Designing positive psychology: Taking stock and moving forward (pp. 293-312). New York: Oxford University Press.

Hilgert, M., A. , Hogarth, J. M., & Beverly, S., G. (2003). Household financial management: The connection between knowledge and behavior. Federal Reserve Bulletin (July), 309-322.

O'Neill, B. (2006). IDA financial education: Qualitative impacts. Journal of Extension [On-line], 44(6). Article 6RIB7. Available at: http://www.joe.org/joe/2006december/rb7.php

O'Neill, B., Xiao, J., Bristow, B., Brennan, P., & Kerbel, C. (2000). Money 2000™: Feedback from and impact on participants. Journal of Extension [On-line], 38(6). Article 6RIB3. Available at: http://www.joe.org/joe/2000december/rb3.php

Osteen, S., Muske, G., & Jones, J. (2007). Financial management education: Its role in changing behavior. Journal of Extension [On-line], 45(3). Article 3RIB2. Available at: http://www.joe.org/joe/2007june/rb2.php

Prochaska, J. O., DiClemente, C. C., & Norcross, J. C. (1992). In search of how people change: Applications to addictive behaviors. American Psychologist, 47(9), 1102-1114.

Robb, C. A., & Woodyard, A. S. (2011). Financial knowledge and best practice behavior. Journal of Financial Counseling and Planning, 22(1), 60-70.

Shockey, S. S., & Seiling, S. B. (2004). Moving into action: Application of the transtheoretical model of behavior change to financial education. Financial Counseling and Planning, 15(1), 41-52.