February 2019

|

February 2019 // Volume 57 // Number 1 // Research In Brief // v57-1rb10

Extension Investing Resources for the Millennial Generation: An Exploratory Study

Abstract

Millennials have different investing knowledge and behaviors than generations in the past. Moreover, as compared to baby boomers, millennials have more debt and less wealth to invest. We used current literature and information collected from Extension educators to explore the values, investing behaviors, learning styles, and loyalty attitudes of millennials. We also examined and evaluated investment resources that had been created or adapted by four Extension faculty members across the nation. A proposed framework with suggestions for future research is provided.

Introduction

As of July 2016 in the United States, the millennial generation, individuals born between 1981 and 1996, was estimated to be around 71 million (Fry, 2018). The number of baby boomers, those born between 1946 and 1964, was estimated at 74 million, and the estimate for generation X'ers, those born between 1965 and 1980, was slightly more than 66 million (Fry, 2018). It has been projected that millennials will outnumber baby boomers as early as this year (Fry, 2018). These changing demographics have implications for Extension professionals who deliver personal finance education. Current investment programs provided through Extension generally have been designed for older generations and may not meet the needs of millennials. Understanding the financial situations of millennials is critical for Extension programming, and generational theory can be used to help explain how generations have formed behavioral characteristics based on their social conditions (Howe & Strauss, 2007). Considering these circumstances, we undertook an exploratory study to broaden the relevant Extension knowledge base by reviewing the behavioral characteristics of millennials specific to finances and investing, examining existing and/or planned Extension investing resources and programming efforts for millennial audiences, and making recommendations for future research on the investing and financial needs of millennials.

Methods

Data Collection and Analysis

We collected data in two phases. First, we conducted an online literature review in February 2017 to ascertain the values, financial and investing behavioral characteristics, learning styles, and loyalty attitudes of millennials. Second, we conducted interviews with four Extension educators currently providing investment resources and programming to determine whether they were providing these resources and programming to millennial audiences. To identify appropriate interviewees, we performed a preliminary online search for Extension investment resources and programming. We found that many Extension educators did not have investment resources listed on their Extension websites, so we widened our search to include retirement resources. On the basis of the 10 websites we found, we requested interviews with four campus-based Extension financial management and planning educators across the United States who had the most investment and retirement resources publicly available; all agreed to be interviewed. Because one of us was very familiar with the work of two of the four educators, the other interviewed these educators to reduce any bias that could exist. We conducted phone interviews that lasted 30–45 min and were focused primarily on investment resources. We recorded responses and then identified and analyzed themes based on the responses. Our interview protocol included seven open-ended questions, along with additional probing questions that were used as needed. The seven primary questions were as follows:

- Please explain what Extension resources you offer related to investing and retirement.

- Did you have a specific target audience in mind when creating the resources?

- When were the resources created, and have they been updated? If so, around what year were they updated?

- Do you have any impact data on the Extension resources that have been created?

- Have you ever provided Extension programming for, or created Extension resources directly targeted to, the millennial generation?

- Do you believe you could alter any of your current Extension resources to better reach a younger workforce/millennials? If so, how?

- If you could create new investment Extension resources, what topics or information would you include, and how would you think about reaching the younger workforce and generation with the resources you think should be created?

Results

Review of Literature

The social and financial lives of millennials differ drastically from those of previous generations. Compared to baby boomers and generation X'ers when they were at the same stage of life, millennials are less likely to be married, be living with a spouse, or have children (Fry, 2017). When adjusted for inflation, the average net wealth of millennials is less than half that of baby boomers when they were of the same age (Young Invincibles, 2017). This circumstance is partly because, as compared to boomers, millennials bring in 20% less income, incur more than twice as much student debt, and have lower rates of homeownership (Fry, 2017; Schultz, 2017). Additionally, the demise of defined-benefit pensions, continued demand for dual-income households, and longer work hours with shorter vacation time have created a generation that values work–life balance more than in the past (Twenge, Campbell, Hoffman, & Lance, 2010).

Numerous national surveys have addressed the financial stability of millennials. A Financial Industry Regulatory Authority (FINRA) report revealed that at the time they were asked, 43% of those aged 18–34 indicated that they would not have an extra $2,000 in the subsequent 30 days to cover an unexpected expense (Lin et al., 2016). Similarly, in a study by Wells Fargo (2016), only half of millennials surveyed had started saving for retirement. It may not be surprising then that a report from Sallie Mae (2016) suggested that 83% of college-aged millennials wanted to learn more about money management, specifically saving.

Not only do millennials spend, save, and invest money differently from past generations, their learning styles differ as well. Compared to baby boomers and generation X'ers, millennials in the United States value social responsibility, work–life balance, teamwork, and the integration of technology to higher degrees (Ertas, 2015; Howe & Strauss, 2007; Hussey, Frazer, & Kopulos, 2016; Lu & Gursoy, 2016; McGlone, Spain, & McGlone, 2011; Murphy, 2012; Twenge et al., 2010). Millennials were the first to grow up in a digital world; integrating technology into a hands-on learning environment is key for educational engagement with this generation (Cavanaugh, Giapponi, & Golden, 2016; Hendrickson et al., 2010; Mangold, 2007; Revell & McCurry, 2010). Millennials learn and retain more information when educational experiences include critical assessment, reflection time, and personal application. This generation expects their learning environment to be team-oriented and interactive (Cavanaugh et al., 2016; Mangold, 2007). For example, researchers used multiple-choice and yes-no questions along with a personal response system (PRS)—an instructional tool comprising a wireless polling system and handheld clickers or personal smartphones—to test student knowledge and found that the use of this form of technology in the classroom increased overall comprehension of material and level of engagement between students and instructors (McCurry, 2014; Revell & McCurry, 2010). Further, Hendrickson et al. (2010) identified podcasts, with the educator's contact information listed, as a positive tool for educating millennials on financial matters.

Millennials, just like generations before, are affected by brand loyalty, a tendency for customers to consecutively purchase or use the same product rather than a competing brand's product (Bowen & McCain, 2015; Gurău, 2012). Bowen and McCain (2015) defined loyal customers as those "who hold positive attitude toward the service provider and also provide repeat purchase behavior" (p. 418). Obviously, a loyal customer must first be a customer. In a study conducted by Adroit Digital, 62% of millennials indicated that the value and price of a product is a priority in choosing a brand; the second most important factor respondents identified was whether the brand had been recommended by a friend (White, 2014). Additionally, 39% of respondents stated that the brand must advertise through the Internet or social media, versus a billboard or radio, to be considered desirable (White, 2014). The changing concepts of attraction to a brand and brand loyalty are important as they relate to a technologically advanced generation that continues to learn through academia, the workplace, and social environments.

Extension Educator Interviews

The Extension educators we interviewed reported that they provided investment education in various formats. Table 1 provides an overview of their responses to questions 1–4 of our interview protocol. Their responses to the remaining questions were overlapping and are summarized in the paragraphs following the table.

| Interviewee | Current resources

(Question 1) |

Target audience

(Question 2) |

Creation and revision

(Question 3) |

Impact data

(Question 4) |

| Educator 1 | Fact sheets and workshops on retirement and estate planning | No specific target audience | Created in 2000s or as needs arose; revised at least every 5 years | No data collected on investment resources. Positive data collected in 2017 on estate planning courses. |

| Educator 2 | News releases, audio interviews, public service announcements, and face-to-face and online investment sessions | Rural, underserved communities | Created in 2008; minor revisions made up to 2015 | 1,000 people have completed online course; precourse/postcourse data collected. Majority of participants have been baby boomers. |

| Educator 3 | Publications, online course, blogs, and news articles on retirement | 50- to 60-year-olds | Created in 2016 | No data collected. There are plans to collect data via preintervention/postintervention evaluation; demographics will not be included. |

| Face-to-face programs and webinars on money management and homeownership | Millennials | Created in 2012 | ||

| Educator 4 | Online courses, monthly articles and webinars, Twitter use, and workshops on investing and retirement | Working-age adults: 22- to 67-year-olds | Created in 2000; revised yearly | No recent data collected. |

Three of the four Extension educators indicated that they had provided financial or investment resources and programming to millennial audiences. All four educators provided suggestions on how best to adapt current resources to target and deliver to millennials. Suggestions included modifying examples to appeal to a younger generation, shortening investment publications, using infographics, and including investing calculators and interactive quizzes in online resources. One educator used Twitter to "chat" about a financial topic with millennials. In this endeavor, she assumed a facilitator role rather than an instructor role and found this teaching style to be beneficial for millennials. The need to integrate other platforms for optimal learning, such as YouTube, Facebook, and podcasts, was also discussed.

Further, Extension educators revealed that citizens, across all generations, have not been attending programs to the same extent as in the past. Specifically, investment programs usually have smaller audiences compared to other family and consumer science programs; the educators were not sure why. To teach millennials about investing, educators suggested collaborating with outside organizations, such as millennial workplaces, to develop lunch-and-learn programs, webinars, and educational programs directly aligned with employer-sponsored retirement plans. Additional suggestions included meeting millennials outside the work environment in both physical and online spaces where they can gather with like-minded peers.

When asked what content should be taught in such an investment program, the educators all expressed the idea that a basic understanding of money management is foundational, regardless of the generation of audience members. Therefore, the importance of budgeting, recognizing needs versus wants, paying off debt, saving for an emergency, and obtaining insurance should be taught first. Most educators also stated the need for millennials to start investing and saving for retirement as soon as possible, either through a tax-deferred savings plan with an employer or an IRA. Educators believed these concepts could be taught by discussing the time value of money and risk diversification.

Discussion

The findings from our examination of the literature on millennials and Extension educator interviews can be examined in the context of three categories pertinent to Extension work: modern learning and delivery techniques, relevant investment content and strategies, and trust of and brand loyalty for Extension.

Modern Learning and Delivery Techniques

Understanding and meeting the millennial audience where they are will be important for Extension educators when creating and delivering investment curricula. For example, a lunch-and-learn program at a company with millennial employees could include PRS technology or other free online platforms, such as Kahoot and Poll Everywhere, to create experiential opportunities that enhance learning. Programs outside the workplace could be provided at locations millennials frequent, such as coffee shops or bars, and via social media outlets such as Instagram and Twitter. Updated and shorter webinars may better meet the needs of millennials, who value work–life balance. Print handouts could be shorter (no more than one page) and could include infographics and charts and suggestions for where to find more information online.

Relevant Investment Content and Strategies

The literature revealed that many millennials have rising debt and very little savings for an emergency. The educators interviewed recommended education on these two topics as a prerequisite to investment education. For millennial audiences ready to open their first investment account, education could be provided on tax-deferred and/or tax-free investment options. Even further, if millennials are looking to expand their current investment portfolios, unbiased and research-based education on risk diversification and different types of investments would be important.

Trust of and Brand Loyalty for Extension Resources

Our research revealed that for Extension to continue as a leader in the field of unbiased, research-based information, millennials, just like generations in the past, must become loyal to Extension. Therefore, if the target customer is the millennial generation, customer loyalty will increase when millennials repeatedly use and/or encourage others to use Extension programs and resources. Millennials must highly value and think positively of Extension to continue attending programs and reading resources, or they will find information through other entities. Both the literature and educator interviews revealed that word-of-mouth recommendations and a presence on social media could be beneficial to the sustainability of Extension's brand.

Conclusions

Ours was an exploratory study, and only limited information can be gleaned from the review of literature on millennials and the interviews with Extension educators. More research on the millennial population is needed before conclusions can be drawn about their investing education needs and how best to reach them. Content on investing and delivery mechanisms best suited for various generations are important not just for family and consumer science programming, but for all Extension program areas. Many parents of 4-H'ers are millennials; thus, 4-H educators can provide these parents with information about Extension investing programs and resources. Such resources can additionally assist millennial farmers and ranchers as they plan for the future of their businesses. For Extension to be the unbiased, researched-based source for every generation, we need to better understand generational differences so that we can deliver information in a relevant and needed way.

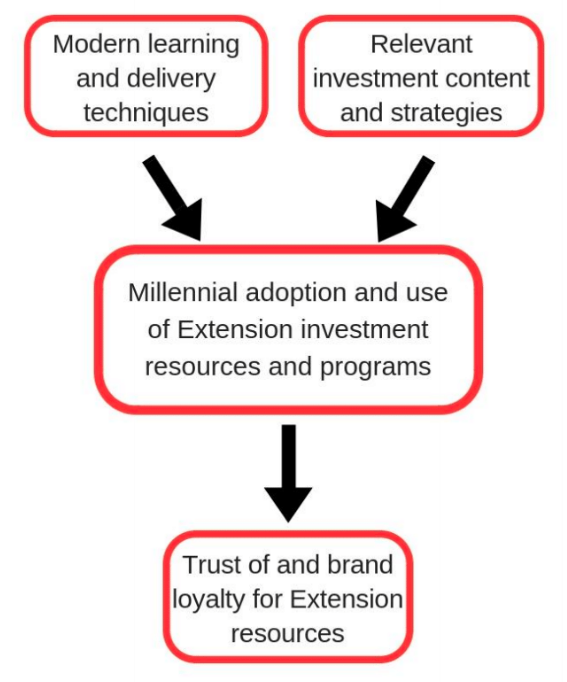

On the basis of the preliminary results we obtained, we propose a framework that can be used as a foundation for future research (see Figure 1). The proposed framework suggests that integrating modern learning and delivery techniques and relevant investment content and strategies into education and outreach for the millennial generation will lead to their adoption and use of Extension investing resources. Through the adoption and use of Extension investing resources and programming, millennials will begin to trust and build brand loyalty for Extension resources and continue to choose Extension for investment education.

Figure 1.

Proposed Framework for Future Research on Investing Resources and Programming Needs of the Millennial Generation

This article does not provide solutions for reaching the millennial generation with Extension investing resources. In fact, one educator interviewed was hesitant to provide any recommendations until talking directly with millennials to determine their needs. Rather, we provide information that can assist researchers with ideas for future research regarding investing education and outreach needs of millennials. Further research conducted by financial planning educators and/or others who study generational differences is needed for providing specific recommendations.

References

Bowen, J., & McCain, S. C. (2015). Transitioning loyalty programs: A commentary on the relationship between customer loyalty and customer satisfaction. International Journal of Contemporary Hospitality Management, 27(3), 415–430.

Cavanaugh, J. M., Giapponi, C. C., & Golden, T. D. (2016). Digital technology and student cognitive development. Journal of Management Education, 40(4), 374–397.

Ertas, N. (2015). Turnover intentions and work motivations of millennial employees in federal service. Public Personnel Management, 44(3), 401–423.

Fry, R. (2017, February 13). Americans are moving at historically low rates, in part because millennials are staying put. Retrieved from http://www.pewresearch.org/fact-tank/2017/02/13/americans-are-moving-at-historically-low-rates-in-part-because-millennials-are-staying-put/

Fry, R. (2018, March 1). Millennials projected to overtake baby boomers as America's largest generation. Retrieved from http://www.pewresearch.org/fact-tank/2016/04/25/millennials-overtake-baby-boomers/

Gurău, C. (2012). A life‐stage analysis of consumer loyalty profile: Comparing generation X and millennial consumers. Journal of Consumer Marketing, 29(2), 103–113.

Hendrickson, L., Jokela, R. H., Gilman, J., Croymans, S., Marczak, M., Zuiker, V. S., & Olson, P. D. (2010). The viability of podcasts in Extension education: Financial education for college students. Journal of Extension, 48(4), Article 4FEA7. Available at: https://www.joe.org/joe/2010august/a7.php

Howe, N., & Strauss, W. (2007). The next 20 years: How customer and workforce attitudes will evolve. Harvard Business Review, 85(7/8), 41–52.

Hussey, L. C., Frazer, C., & Kopulos, M. I. (2016). Impact of health literacy levels in educating pregnant millennial women. International Journal of Childbirth Education, 31(3), 13–18.

Lin, J. T., Bumcrot, C., Ulicny, T., Lusardi, A., Mottola, G., Kieffer, C., & Walsh, G. (2016). Financial capability in the United States 2016. Retrieved from the FINRA Investor Education Foundation website: https://www.usfinancialcapability.org/downloads/NFCS_2015_Report_Natl_Findings.pdf

Lu, A. C., & Gursoy, D. (2016). Impact of job burnout on satisfaction and turnover intention. Journal of Hospitality & Tourism Research, 40(2), 210–235.

Mangold, K. (2007). Educating a new generation. Nurse Educator, 32(1), 21–23.

McCurry, M. K. (2014). The great American cookie experiment updated for the millennial learner. Journal of Nursing Education, 53(3), 180–180.

McGlone, T., Spain, J. W., & McGlone, V. (2011). Corporate social responsibility and the millennials. Journal of Education for Business, 86(4), 195–200.

Murphy, W. M. (2012). Reverse mentoring at work: Fostering cross-generational learning and developing millennial leaders. Human Resource Management, 51(4), 549–573.

Revell, S. M., & McCurry, M. K. (2010). Engaging millennial learners: Effectiveness of personal response system technology with nursing students in small and large classrooms. Journal of Nursing Education, 49(5), 272–275.

Sallie Mae. (2016). Majoring in money: How American college students manage their finances. Retrieved from the Sallie Mae website: http://news.salliemae.com/sites/salliemae.newshq.businesswire.com/files/doc_library/file/SallieMae_MajoringinMoney_2016.pdf

Schultz, A. (2017, January 13). Here's proof that millennials have yet to find their financial footing. Barron's. Retrieved from http://www.barrons.com/articles/heres-proof-that-millennials-have-yet-to-find-their-financial-footing-1484352509

Twenge, J. M., Campbell, S. M., Hoffman, B. J., & Lance, C. E. (2010). Generational differences in work values: Leisure and extrinsic values increasing, social and intrinsic values decreasing. Journal of Management, 36(5), 1117–1142.

Wells Fargo. (2016). 2016 Wells Fargo millennial study. Retrieved from https://www08.wellsfargomedia.com/assets/pdf/commercial/retirement-employee-benefits/perspectives/2016-millennial-retirement-study.pdf

White, R. (2014, September). Millennial brand loyalty still going strong. Credit Union Times, 25(34), 12. Retrieved from Business Source Complete.

Young Invincibles. (2017). Financial health of young America: Measuring generational declines between baby boomers and millennials. http://younginvincibles.org/wp-content/uploads/2017/04/FHYA-Final2017-1-1.pdf