February 2018

|

February 2018 // Volume 56 // Number 1 // Tools of the Trade // v56-1tt1

Using Simulated Farm Case Studies to Teach Financial and Risk Management Concepts

Abstract

Two simulated farm case studies provide a means for teaching financial and risk management strategies to western Kentucky grain farmers. Aggregate financial data for 227 grain farms define the case studies, which illustrate how cost and debt affect cash flow and working capital over a 5-year period. Responding to the case studies, farmers were able to discuss these financial concepts in a group setting among competitor neighbors without revealing personal business information. The use of composite financial data engaged the farmers and allowed for improved discussion on risk management products and the potential to protect working capital over multiple years. Extension professionals can apply the methods described.

Introduction

Teaching financial and risk management concepts to farmers is challenging as the best strategy depends on comparing unique cost structure, debt level, family living expense, and available working capital data to price, yield, financial risk, and the individual farmer's risk tolerance. Consequently, Extension management educational programs often involve the use of decision aids that provide farmers with a range of outcomes. Farmers then determine where they are on a continuum of possible cost structures and debt levels to choose the best strategy.

A second issue related to delivering precise financial and risk management education is that farmers can be hesitant to disclose cash rental rates, machinery costs, and family living expenses in a group setting. One strategy for circumventing this hesitance is to use case studies. For example, Barnard (1996) used a case study to teach financial statements in a workshop setting and reported that students experienced an engaged learning environment. Building on Barnard's methodology, we developed simulated farm case studies from real aggregate farm-level data and used those case studies to teach financial and risk management concepts to grain farmers and agricultural lenders in a workshop setting.

Development and Use of Simulated Farm Case Studies

Kentucky Farm Business Management program data summarizing 227 grain farms (Jenkins, 2015) were the source for our simulated farm case studies. The two case studies represent a low-cost/low-debt (LCLD) grain operation and a high-cost/high-debt (HCHD) grain operation. These farms bookend a continuum of possible cost and debt structures. In using the case studies to discuss scenarios with farmers, our assumptions included

- identical production variables for both farms and

- identical acreage, crop mix, yields, and market prices.

We kept these variables constant to focus the discussion on managing cost, debt, and working capital.

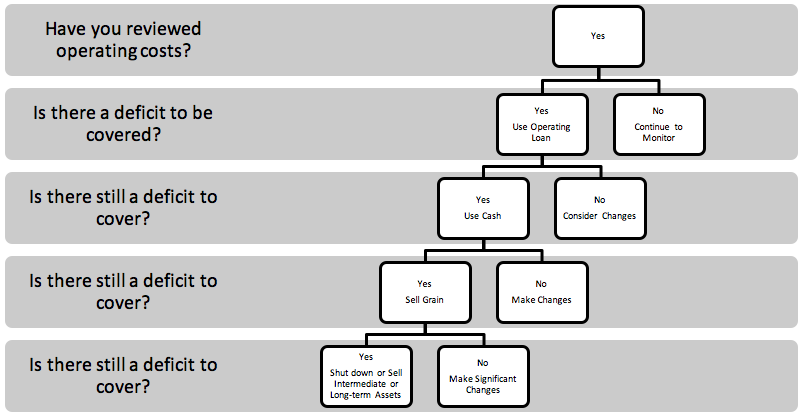

The financial and risk management model we used with the case studies simulated each farm business's cash flow for 2016 to 2020. The cash flow included production costs, land rent, overhead expenses, family living withdrawals, principal and interest payments for the operating note, and principal and interest due on intermediate and long-term debt. Figure 1 shows how the model addressed cash flow deficits. According to the model, if the farm business had a deficit, the farmer's first step would be to increase operating note borrowing to manage the deficit. Following that step, the farmer would use cash to pay any deficit remaining after reaching the operating debt limit and then income from additional grain sales to pay any deficit remaining after using debt and cash. The model stopped if the farm's working capital was exhausted, and we asked the audience to suggest managerial alternatives for dealing with remaining cash flow problems. Suggestions included selling intermediate or long-term assets, liquidating personal retirement accounts, and converting current debt to long-term debt.

Figure 1.

Simulated Farm Deficit Management Strategy

Benefits of Using Simulated Farm Case Studies in Extension Education

The case studies engaged farmers in a nonthreatening and less personal discussion. Farmers could discuss risk management strategies without revealing to potential rivals their own cost structures, debt levels, or amounts spent on family living. Farmers used Turning Point clickers to answer questions anonymously about possible managerial solutions to problems illustrated by the case studies.

The farm case studies have specific financial and risk management lessons embedded in their design. The workshop focus was on managing cost, debt, and working capital and using appropriate risk management tools for the 2016 crop year. The two extreme farm case studies illustrated that risk management is farm and farmer dependent. The ideal risk management plan depends on the farmer's willingness to accept the risk of a cash flow deficit. Some farmers may use risk management tools to reduce the risk of maximizing operating credit or liquidating cash and grain reserves.

The simulated farm case studies illustrate the interaction between risk management tools and a farm's financial position. Many Extension programs do not address the complementary effects of combining risk tools to protect revenue. The effects of risk management on a farm's finances are not taught in Extension meetings. As many grain farms in western Kentucky have cash flow problems instead of debt, workshop emphasis was on ensuring that farmers understood the risk management tools available for preserving working capital over a multiyear period.

Discussion Generated by Simulated Farm Case Studies

The HCHD farm exhausted working capital before the end of the 5-year simulation. The resulting discussion centered on modifying cash rental rates, machinery costs, and family living expenses to reduce cost structure.

Farmers discussed whether paying a premium for marginal ground is worth the benefit of reducing fixed costs. Many farmers indicated fearing that they might never have the opportunity to rent the ground again as others could be willing to pay higher rental rates. Farmers noted that landowners are less sympathetic about reducing cash rental rates for farmers who have not reduced family living expenses.

The machinery cost discussion alerted farmers to the tax consequences of selling machinery written off under Section 179 expensing. Specialists involved in the workshops also reminded farmers that reducing machinery capacity might slow the timeliness of planting and harvesting, resulting in yield penalties and lower profitability.

The final discussion point was family living expenses. The average family living expense in 2014 was $108,550 (Pierce, 2016). The consensus was that reducing family living expenses is difficult because reductions are likely to cause stress as family members have to sacrifice more than in previous years.

Additional discussion focused on risk protection. The farm case studies illustrated the risk protection provided by revenue protection crop insurance, hedging with futures, put options, and forward contracts for the 2016 crop year. The farm case studies also illustrated the risk protection provided by combining these risk management tools for both the LCLD and HCHD farms.

Lessons Learned and Suggestions for the Future

One lesson we learned is that agricultural lenders should be involved in creating the case studies and participating in the workshop discussions. Another is that discussions should be oriented specifically toward beginning farmers. These farmers may have higher debt and higher costs than more established farmers. Additionally, beginning farmers who have not experienced commodity cycles may have unrealistic expectations of farm profitability and use of risk management tools to protect revenue risk.

In a future version of the financial and risk management educational programming, we will use the Kentucky Farm Business Management data to develop case studies of farms with top-third, middle-third, and lowest-third profitability levels to provide further detail regarding the continuum of cost structures and debt facing western Kentucky grain farmers. In general, Extension specialists working with farmers elsewhere can apply the simulated-farm-case-studies method to teach financial management and risk management concepts and engage farmers without asking for personal financial information.

References

Barnard, F. L. (1996). PASSing the Financial Management Interest Exam. Journal of Extension, 34(4), Article 4TOT1. Available at: https://www.joe.org/joe/1996august/tt1.php

Jenkins, A. (2015). Annual summary data—Kentucky grain farms—2014. Retrieved from http://www.uky.edu/Ag/AgEcon/pubs/kfbmkfbmsumgr201410.pdf

Pierce, J. S. Jr. (2016). Preliminary grain analysis summary. Retrieved from http://www.uky.edu/Ag/AgEcon/pubs/extkfbmsumdata1627.pdf