June 2016

|

June 2016 // Volume 54 // Number 3 // Ideas at Work // v54-3iw5

Credit Score Millionaire: An Innovative Program Helps Diverse Audiences Build Strong Credit Scores

Abstract

Local and statewide needs assessments resulted in an emerging priority to prepare teens to build strong credit scores and avoid some common missteps of establishing credit on reaching adulthood. The resulting Credit Score Millionaire program was developed through the use of innovative technologies and instructional design concepts to deliver face-to-face programming to nearly 2,000 participants and indirectly reach thousands more through online and train-the-trainer delivery methods. The objectives of the program were to promote low-cost/high-impact strategies for building strong personal credit. Participants have reported significant increases in understanding of personal credit scores and plans to improve credit-related decisions.

Background

In recent years, a variety of Extension programs have addressed the concept of using personal credit wisely as part of an overall plan to achieve financial success (Bobbit, Bowen, Kuleck, & Taverno, 2012; Osteen, Muske, & Jones, 2007; St. Pierre & Shreffler, 2013). However, few Extension programs have focused directly on credit score education. A credit score is a numerical indicator of a consumer's "creditworthiness." It is determined by credit scoring agencies through mathematical algorithms that weight past loans and payment activities listed on an individual's credit report. There are several private companies that produce credit scores, but the credit score used in over 90% of all consumer credit checks is called the FICO classic score, a name that refers to either the FICO 04 proprietary scoring model or the FICO 8 proprietary scoring model (Bingham, 2011; MyFico, 2015).

National Public Radio reported that a credit score can be just as important as an SAT score for youth who are transitioning to adulthood (Horsley, 2006). This is because credit reports and credit scores are no longer used exclusively by lenders but also are used by insurance companies, landlords, utility companies, elective medical service providers, and even employers to make critical decisions on individuals. For example, the difference between a score of 808 and a score of 638 (170 points) costs the average consumer about $1,000 a month in increased borrowing and insurance costs (Bingham, 2011).

Program Description

Local and statewide needs assessments identified credit score education for youth and young adults as an emerging priority. The objectives of the resulting program were to promote positive financial behavior change and low-cost strategies for establishing and building strong personal credit. Literature indicates that increased wealth and productivity resulting from increased credit scores ultimately strengthens the economy and reduces dependence on government and community nonprofit organizations (Fellowes, 2009).

University of Idaho Extension educators created and disseminated the two-part program Credit Score Millionaire. The first part of the program delivered fundamental credit score concepts through a video presentation having graphics and animation produced through the use of web-based software called PowToons. The second part of the program asked learners to review and build on the content from the first part by participating in a game show–type activity titled "Who Wants to be a Credit Score Millionaire?" This activity was built in PowerPoint through the use of dynamic hyperlink navigation and engaging audio and graphics.

The primary audience for the program was high school seniors. Classes were taught to high school audiences, and workshops were held to train high school teachers and other youth leaders on how to administer the program.

Program Expansion

The Credit Score Millionaire program has been adapted for group use as well as for individual web users. Also, materials have been made available for download (http://northwestyouthfinancialeducation.org/educators-credit-score-millionaire) for free use by other educators. Detailed instructor guides are included so that even novice instructors can effectively share this program with youth. Also available for download are program marketing materials and evaluation tools.

The Credit Score Millionaire program has already proven, in a relatively short time, to be of significant interest to audiences and partners from a variety of disciplines. Original plans for program development called for targeting 4-H youth and high school students, but the program subsequently was expanded to reach audiences such as civic groups, senior citizens, college students, farmers, job seekers, and learners with disabilities. The program has been delivered directly and indirectly through the use of a train-the-trainer model, which leverages the time and skills of other youth leaders.

Impact

To date, the total number of direct face-to-face program participants is 1,919 (685 adults and 1,234 youth). It is estimated that hundreds more have been reached indirectly by educators who have been trained to offer this program themselves. Web materials registered 1,117 hits/downloads over a period of about 18 months. The Credit Score Millionaire program also has been featured by a variety of media outlets, including ABC affiliate KIFI, which reaches the Eastern Idaho/Western Wyoming market area of 126,150 homes (The Nielsen Co., 2013). Online and paper-based evaluation tools were developed to capture retrospective self-assessment data from program participants. Adult participant self-assessment data showed an approximate average 40% increase in areas of knowledge, confidence, and intended behavior improvement with regard to credit scores. Youth participant self-assessment data showed an approximate average 45% increase in areas of knowledge, confidence, and intended behavior improvement with regard to credit scores.

Adult participants were asked to state something they planned to do as a result of program participation. Responses included the following statement excerpts:

- "not use a finance company for any more purchasing";

- "pull my credit report and look for errors";

- "pay down my credit card";

- "use information in my classes, the six industries which utilize credit scores"; and

- "[in my classes] I plan to go over the five factors in determining your FICO credit score."

Youth participants also were asked what they planned to do after participating in the program. Responses included the following statement excerpts:

- "build [a] good credit score by paying my debts,"

- "never get a bankruptcy,"

- "be smart and don't miss a payment,"

- "build my credit score when I am in college," and

- "try not let my score get below 760."

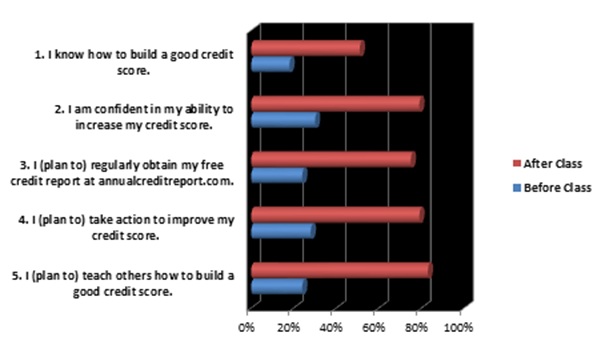

At the conclusion of each workshop, participants were asked to recall the knowledge they had and behaviors they engaged in before the workshop and make comparisons to their knowledge and intentions for behavior after workshop participation (retrospective survey). See Figures 1 and 2 for survey results.

Figure 1.

Credit Score Millionaire: Retrospective Survey Adult Participant Responses

Figure 2.

Credit Score Millionaire: Retrospective Survey Youth Participant Responses

Conclusion

The Credit Score Millionaire program is among the few existing Extension resources that focus primarily on helping youth and adult participants build credit scores. Participants in the program reported significant gains in understanding of credit scores and plans to make improvements to their own scores. Literature suggests that as a result program participants will pay less for future loans, insurance, elective medical procedures, and apartment rentals and will have better employment opportunities (Bingham, 2011; Horsley, 2006). In terms of public value, such effects can be expected to increase the strength of local economies and reduce dependence on government and community programs (Fellowes, 2009). In addition to having participant and societal impacts, the Credit Score Millionaire program is an example of unique program design and delivery based on an interactive game format for both personal online use and group presentations. Also, it has been made available on the web for other educators to download and use for free. As a way to gauge knowledge acquisition and behavior change resulting from the program, consumers can obtain their credit scores for free as a value-added service from most creditors when applying for new credit.

References

Bingham, A. (2011). The road to 850: Proven strategies for increasing your FICO credit scores. Layton, UT: CP Publishing.

Bobbit, E., Bowen, C., Kuleck, R., & Taverno, R. (2012) Volunteer income tax assistance programs and taxpayer actions to improve personal finances. Journal of Extension [online], 50(4) Article 4RIB9. Available at: http://www.joe.org/joe/2012august/rb9.php

Fellowes, M. (2009). Credit scores, reports, and getting ahead in America. The Brookings Institution.

Horsley, S. (2006). Credit scores as important to teens as SATs. National Public Radio. Retrieved June 25, 2015, from http://www.npr.org/templates/story/story.php?storyId=5416319

MyFico. (2015). Credit basics. Retrieved June 25, 2015, from http://www.myfico.com/CreditEducation/articles/

Osteen, S., Muske, G., & Jones, J. (2007). Financial management education: Its role in changing behavior. Journal of Extension [online], 45(3) Article 3RIB2. Available at: http://www.joe.org/joe/2007june/rb2.php

St. Pierre, E., & Shreffler, K. (2013). Credit card usage among older adults: Assessing financial literacy and pressures. Journal of Extension [online], 51(3) Article 3RIB5. Available at: http://www.joe.org/joe/2013june/rb5.php

The Nielson Company. (2013). Local television market universe estimates. Retrieved June 25, 2015, from http://www.nielsen.com/content/dam/corporate/us/en/docs/solutions/measurement/television/2013-2014-DMA-Ranks.pdf