February 2015

|

February 2015 // Volume 53 // Number 1 // Feature // v53-1a7

Creating a Model for Successful Microenterprise Development (MED) Programs

Abstract

Communities seek to offer effective financing programs to encourage entrepreneurs and support the growth of microenterprises. Community economic development strategies have changed in recent years from traditional industrial recruitment to microenterprise development (MED), which is considered to be as a more viable, long-term strategy to create jobs and grow local economies. This article provides a framework for an effective microenterprise financing program based on the model created by a rural community in Ohio and offers suggestions as to how this framework may be used by researchers and practitioners to identify best practices in the microenterprise financing realm.

Introduction, Problem Statement, and Objectives

Microenterprise exists in every community in the United States. From the downtown stores and restaurants to the machine shops or construction businesses, microenterprise is there, providing an income for millions of families and creating greatly needed jobs in urban and rural communities. For some entrepreneurs, their idea is good, and the market exists. But capital is out of reach, and supportive services are not available.

The Small Business Administration (SBA) indicates that about one-third of new employer establishments fail within 2 years, and only half survive at least 5 years (SBA, 2012). In order to assist small establishments struggling to succeed, Extension has engaged in numerous forms of outreach over the years as part of its community economic development mission. One form of engagement that has potential in helping small businesses while achieving community development goals is the microenterprise development program (MED).

The MED movement has grown in response to unemployment and poverty in the United States (Clark & Kays, 1999; Schmidt, Kolodinsky, Flint, & Whitney, 2006). Many local communities are turning to indigenous development strategies, such as microenterprise-centered economic development (Christy, Wenner, & Dassie, 2000).

Vehicles to provide microenterprise loan funds and supportive services can be established within communities to assist small businesses in getting started. This article presents a model developed by Ohio State University Extension in Van Wert, Ohio to establish a microenterprise financing program based on best practices learned from other microenterprise entities in the Midwest region. The objectives are to: (1) set forth a framework for a successful microenterprise model that can be replicated by other communities and (2) encourage and guide researchers and practitioners toward further study of best practices based on the principles set forth in the framework outlined in this article.

Overview of Microenterprise Programs

The Association for Enterprise Opportunity (AEO, the national trade association for microenterprise development organizations) defines a microenterprise as a business that has five or fewer employees and requires $35,000 or less in start-up capital (AEO 2013). AEO estimates that more than 20 million microenterprises are operating in the United States and that microenterprise employment represents 16.6% of all private (non-farm) employment in the country. The impact of microenterprise on employment and contribution to the national economy is substantial (AEO 2008).

MED programs in the United States are extremely diverse. They differ in their goals, strategies, target populations, size, and sources of funding (Glackin & Mahony, 2002). Many of these diverse programs exist within the Midwest region, with some having a much better track record than others in numbers of loans, success rates, and program viability, visibility, and sustainability. Certain management and design characteristics are common among most microenterprise programs.

The majority of microenterprise programs are managed by public entities or not-for-profits whose mission is to stimulate the growth of small enterprises in their community, eliminating poverty and building local economic vitality. This goal is accomplished by offering direct technical assistance and support to local entrepreneurs and by providing financing needed to enable microenterprise projects to go forward. Microenterprise financing usually fills the gap between the limited funds that the entrepreneur has available and the total cost of the project. Micro-funds are typically available for just about any purpose: machinery or equipment, building acquisition, new construction, remodeling, inventory, and working capital.

Non-profit lending groups are often confused about the nuts and bolts of establishing and managing a successful microenterprise program. Their boards are most often comprised of volunteers, many of whom do not have in depth experience in financial analysis, loan structuring, business support, or technical assistance and how these components interact. Oftentimes board members' motivations are based on social as well as economic values; they endeavor to assist lower income entrepreneurs to create their own independent sources of income. Considerations such as board structure and involvement, loan fund policies and procedures, and program management and staffing are not issues with which they are familiar. Currently no one place provides information about these topics, so it is difficult for microenterprise boards and managers to identify structures, policies, and processes that will offer a better chance to establish and operate a successful microenterprise program.

Microenterprise loan programs are an important component of a well-rounded MED program and are usually initiated when a public entity such as a city or county, or a not-for-profit corporation determines that microenterprise financing is a needed strategy to achieve their community's economic development goals. The lead entity usually applies for a grant or other funding to "seed" the loan fund. The initial grant is loaned out and revolves back to the entity as principal, and interest payments are received back into the fund from the borrowers. As the loan fund grows, additional grants may be requested in order to maintain an adequate balance available to lend out to new applicants. Once the loan fund reaches a certain level, it can become self-supporting through loan payments and is likely not to need a new infusion of funds. A certain percentage of loan paybacks can be used as an administrative fee to cover costs of loan fund management. Program sustainability—the ability to remain viable over time—is one critical measure of success of a microenterprise loan program.

A typical microenterprise loan fund can provide all or almost all of the financing needed by entrepreneurs to implement their projects. This is different from traditional publically managed loan programs that usually will only fund up to 50% of a project, with the gap filled by bank loans and owner equity. In contrast, although encouraged, no cash is required from the microenterprise borrower, other than a nominal application fee, usually between $25 and $100. Some form of new or existing collateral is usually required as loan security, and the type of collateral allowable includes items, such as automobiles, that would not be allowable under more traditional programs. Loans are smaller, usually capped at no more than $20,000 per loan. Programs allow applicants to borrow money at or below market interest rates for reasonable terms, usually between 1 to 7 years, depending on what the loan is intended to finance. Some programs, depending on the source of the seed funds, will require applicants to be income eligible in order to apply.

The Van Wert County, Ohio Model

Getting Started: Community Sustainability Goals

Local Extension offices can often be key players in both identifying the small business community and providing education and support to further develop the microenterprise segment of the local economy (Muske, Woods, Swinney, & Khoo, 2007). Extension's potential role in MED can range from training community development entities to create and manage a program to providing services directly. In Van Wert County, Ohio, the Extension Community Economic Development office chose to become directly involved with the establishment and management of MED. Extension committed to this more engaged role in order to create a vehicle that would further community sustainability goals Extension and local program organizers identified five community sustainability goals that could be addressed through microenterprise development strategies (Table 1).

| Sustainability Goals | Strategies | Baseline Indicators (2010 census) |

| 1. Stem population decline | Create new jobs in order to stabilize and increase population | Van Wert had a population of 29,659 persons in 2000, representing a decrease of 799 people, or 2.3% from 30,458 in 1980. Ohio Development Services Agency Office of Research predicts that population will continue to decrease to 28,180 by 2015. |

| 2. Retain/recruit youth and seniors |

a. Encourage youth and seniors to startup businesses b. Attract/retain youth and seniors interested in opening businesses |

Van Wert has an older median age, 36.2 years, compared to 35.5 years for the state and 34.9 for the nation. |

| 3. Increase household income |

a. Boost household income by promoting entrepreneurial opportunities b. Increase household income through supplemental business income opportunities |

Mean household income in Van Wert County in 2000 was $35,491, well below the state ($39,454) and the nation ($43,458). Median household income was $35,000 per year, indicating underemployment and entrepreneurship potential. |

| 4. Diversify the local economy | Increase entrepreneurial opportunities to decrease dependence on manufacturing employment | Van Wert's employment base is heavily dependent upon the auto industry; 41% of the workforce is employed in manufacturing, vs. 21% for the state, 15% nationally. |

| 5. Grow gap sectors |

a. Grow the service sector of the local economy b. Build on the strong agricultural base through creation of biosciences businesses. |

Van Wert's services sector is well below national and state averages |

With the understanding that there are no quick fixes, the outcomes listed in Table 1 were identified as long-term sustainability goals that with strategic and unabated effort could be achieved over time.

Establishing a Microenterprise Loan Program

In 2000 the Ohio State University Extension Community Economic Development (Extension CED) Office in Van Wert County initiated a microenterprise loan program at the request of local government leaders. The primary purpose of the proposed loan fund was to create private sector job opportunities principally for underserved populations or persons of low-and-moderate-income (LMI) within the county, adding a recognized needed dimension to the county's overall Economic Development Program (Bowen-Ellzey, 2014).

In establishing the loan program, Extension CED and program organizers were initially tasked with identifying best practices from other microenterprise programs in Ohio and the Midwest region. Organizers conducted a series of eight face-to-face meetings and 20 telephone interviews with microenterprise program board members and managers over the space of 12 months. Programs were identified based on longevity, referral, and publicized success. Extension CED organizers requested input to define program elements that are most important in the operation of a successful loan program.

Elements of a Comprehensive Program

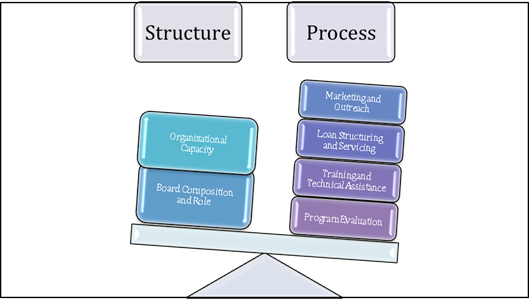

During this discovery phase, it became clear to Van Wert organizers that for a loan program to be successful and sustainable, it needed to be comprehensive. A successful program should incorporate components beyond a stand-alone loan program to include a deeper client support system and a management structure that could stand the test of time. Extension initiated an analysis of numerous MED programs to identify explicitly the characteristics that appeared to be present in those programs that had shown success in achieving the goals set out in Table 1. This informal research into best practices prompted Van Wert County program organizers to opt for a comprehensive MED program that incorporated the elements outlined in Figure 1.

Figure 1.

Model MED Program: Balance of Structure and Process

Note that the characteristics that emerged can be conceptualized as falling into one of two categories: structure and process. Descriptions of the elements within each category are as follows.

- Organizational capacity. The majority of successful MED programs were housed within public or not-for-profit organizations with adequate staff and expertise. Many of the organizations were structured as 501(c)(3) tax-exempt organizations for the purpose of applying for certain grants or to encourage private donations to help support the program. Successful MED programs also had a staff person or persons with dedicated responsibility and competency to manage the program.

- Board composition and role: Based on informal research, an effective board appears to be one of the most critical elements of a successful MED program. A broad-based board should include not only representation from the business and finance community but also from social services and religious and/or outreach organizations within the community. This diversity of interests helps to blend sound financial decision making with sensitivity to the target clientele of lower income persons. Effective boards have committed volunteers willing to dedicate time to serving on the board in addition to acting in an advisory capacity for staff and clients. They possess sought-after skills needed to actively engage in program delivery, technical assistance, and evaluation.

- Marketing and outreach. Successful MED programs celebrate new business creation and client successes. New businesses are publically celebrated through events and news releases, promoting the individual business while marketing the overall loan program to potential applicants. Borrower testimonials and publicity at loan closings are very effective ways to market the program. The financial services community is also recruited to help market the program through initial client screening and referrals. Staff and board members target specific markets to deliver presentations about program and advertise regularly in a variety of local print and online venues.

- Loan structuring and servicing. At the core of any MED program is a loan structure and servicing component that provides a balance between simplicity and fiscal responsibility. Loan processes should not be so complicated and time-consuming as to discourage new clients. On the other hand, loan-structuring policies, including loan size, rate and term structure, and collateral requirements should be well conceived and appropriate for the clientele. Loan requirements can either encourage or stifle microenterprise development.

- Training and technical assistance. From conversations with people involved with successful microenterprise programs, Extension CED came to understand the critical role of training and technical assistance, not only during the loan submission process but also after business launch, in order to enhance the likelihood of success for clients. Types of technical assistance that were identified as important to provide to microenterprises included one-on-one consultation and mobile classrooms in addition to a number of Web-based training media such as webinars and YouTube videos. Volunteer training is essential to augment staff time to assure positive outcomes. To serve on the board and assist clients, volunteers should be required to receive mandatory annual training and review of loan fund practices.

- Program evaluation. It became very clear in reviewing programs throughout the Midwest that developing a method for evaluating progress and metrics for success will keep the program on track over time. Managing board volunteers, the client base, record keeping, and reporting metrics were recognized during interviews as crucial functions of a successful MED program. Evaluation measures and methods to ensure program sustainability are outlined in Table 2.

| Program Element | Evaluation Criteria | Evaluation/ Method |

| Organizational Capacity | Organization has adequate capacity, including staff expertise, financial resources, community support and partnerships, for successful delivery of services. | Annual evaluation |

| Board Effectiveness | Board represents community diversity and includes volunteers who bring expertise and dedication, committing resources to assist staff and clients. | Board training annual review |

| Marketing and Outreach | Staff and board are using a variety of methods to market and outreach to nontraditional populations including under and unemployed and students. | Annual report/success metrics |

| Loan Structuring and Servicing | Loan structuring policies are clearly articulated and not complicated. Staff and board are coordinating client follow-up and monitoring roles are described and well understood. | Updated policy and procedures |

| Training and Technical Assistance | Organization offers a variety of opportunities for training and technical assistance. Board is required to engage in providing consultation as needed. | Annual report/success metrics |

| Program Evaluation | The MED program is evaluated on an annual basis to measure ongoing results and to determine if the program is achieving desired outcomes. | Annual report/success metrics |

MED program success is ultimately measured by program outcomes and impacts. Extension CED and board members identified seven success metrics that would be measured annually to determine if the program was having an impact. From startup of the program in 2000 through 2012, when staff changes occurred in the Extension CED office, these metrics were measured with results listed in Table 3.

| Outcome | Impact |

| Number of individuals enrolling in training | 2,775 |

| Number of individuals completing training | 1,910 |

| Number of individuals applying for loans | 220 |

| Number of individuals receiving loans | 88 |

| Dollars loaned | $3M |

| Number of business starts | 65 |

| Number of jobs created/retained | 350 |

In the dozen years during which metrics were measured for the Van Wert MED program, almost 2,000 people completed entrepreneurship training, averaging about 160 people per year. While 220 individuals applied for loans, 88, or 40%, of individuals who applied actually received one. These 88 new businesses created an average of about four jobs each for a total of 350 jobs during this 12-year time frame. Based on a conservative multiplier of 0.5 additional jobs created for every one job generated as a result of the MED program (Blaine, Bowen-Ellzey, & Davis, 2011), the Van Wert community benefited from a total of 525 jobs created. Because loans were made based on sound loan policies and in accordance with community sustainability goals, most of the jobs created helped grow new businesses that diversify the economy by filling gaps that existed in the marketplace.

Replicating the Van Wert Model in Your Community

Using the framework that has been set forth through the Van Wert County model, it is possible for interested researchers and practitioners to adopt, use, and measure the success of microenterprise loan programs. Using qualitative and quantitative research approaches, researchers can identify key indicators of success, including elements of a loan program that will have a greater likelihood of success for communities and entrepreneurs. On-line surveys, key informant interviews, and the measurement of loan completion data will be used to determine the level of effectiveness of loan programs and to define a best practices model that can be articulated and shared for replication.

Although many microenterprise programs exist within the Midwest region, some have a much better track record than others in numbers of loans, success rates, and program viability, visibility, and sustainability. Nonprofit community development organizations and public entities that operate MED programs have the experience and knowledge base and would provide good input for the study. Results of the information gathering and follow-up analysis reported here can help provide the structure and process needed to produce the kind of comprehensive program that leads to the achievement of community economic development goals.

Conclusions and Suggestions for Further Research

Promoting entrepreneurship is an important goal of most communities. Local governments and community development entities are seeking ways to assist and encourage entrepreneurship and microenterprise development. A successful program merges best practices to provide communities with a tool that can have measurable impact on local economies in terms of job creation and serve as an important catalyst for increased prosperity and economic development. Policy makers can gain from a more unified perspective on how studies and samples fit together (Kerr & Nanda, 2009).

Toward that end, the study reported here (1) offers an operational model of a successful MED program that incorporates an informal review of best practices in its development, management, and operations and (2) describes how these best practices were applied to the creation of a microenterprise program in Van Wert, Ohio. The model features a balance between structure and process, and identifies the key features of each.

The authors encourage researchers and practitioners alike to gain a deeper understanding of all the components of microenterprise programs. This will require work (a) to identify critical factors of success and (b) to develop additional methodologies that will provide guidance to public entities and not-for-profits as they establish and operationalize microenterprise loan funds in their communities. More intensive qualitative and quantitative research needs to be conducted in order (a) to measure the extent to which various factors determine loan program sustainability and (b) to refine a replicable model for microenterprise loan programs that can provide guidance to communities seeking to achieve economic development goals.

References

Association for Enterprise Opportunity. Catalyst initiative. Retrieved from: http://www.aeoworks.org

Blaine, T. W., Bowen-Ellzey, N., & Davis, G. A. (2011). Helping clientele understand elements of the local economy through input-output modeling. Journal of Extension [On-line], 49(1) Article 1FEA5. Available at: http://www.joe.org/joe/2008april/a1.php

Bowen-Ellzey, N. (2014). Microenterprise development program encourages entrepreneurship while supporting Extension in Van Wert County, Ohio. Journal of Extension [On-line], 52(2) Article 2IAW5. Available at: http://joe.org/joe/2014april/iw5.php

Christy, R., Wenner, M., & Dassie, W. (2000). A microenterprise-centered economic development strategy for the rural south: Sustaining growth with economic opportunity. Journal of Agricultural and Applied Economics, 32(2), 331-344. Retrieved from: http://ageconsearch.umn.edu/bitstream/15489/1/32020331.pdf

Clark, P., & Kays, A.J. (1999). Microenterprise and the poor: findings from the self-employment learning project five year study of microentrepreneurs. Washington, DC: The Aspen Institute.

Glackin, C. E. W., & Mahony, E. G. (2002). Savings and credit for U.S. micro-enterprises: Individual development accounts and loans for microenterprise. Journal of Microfinance 4(2): 93-125.

Kerr, W., & Nanda, R. (2009). Financing constraints and entrepreneurship. Harvard Business School Working Paper.

Muske, G., Woods, M., Swinney, J., & Khoo, C. (2007). Small businesses and the community: Their role and importance within a state's economy. Journal of Extension [On-line], 45(1) Article 1RIB4. Available at: http://www.joe.org/joe/2007february/rb4.php

Ohio Development Services Agency Office of Research (2014). Population Characteristics and Projections Retrieved from: https://development.ohio.gov/reports/reports_pop_proj_map.htm.

Schmidt, M., Kolodinsky, J., Flint, C., & Whitney, B. (2006). The impact of microenterprise development training on low income clients. Journal of Extension [On-line], 44(2) Article 2FEA1. Available at: http://www.joe.org/joe/2006april/a1.php

Small Business Administration (2012). Small business facts. Retrieved from: http://www.sba.gov/sites/default/files/Business-Survival.pdf