February 2013

|

February 2013 // Volume 51 // Number 1 // Tools of the Trade // v51-1tt6

Teaching Financial Literacy Across the Generations

Abstract

This article describes a tool developed by educators of the University of Minnesota Extension and University of Wisconsin Cooperative Extension to assist professionals as they plan financial education for participants. In today's changing economy, financial education is essential throughout one's life cycle. By understanding learner attributes, educators can create motivating learning environments and seek appropriate teaching methods to capture participant attention. Multi-generational complications may arise as people view and communicate about money differently. The financial literacy grid was developed to examine generational characteristics, life cycle tasks, financial concepts, and appropriate teaching techniques to meet learner needs.

Introduction

In today's changing economy, financial education is essential throughout one's life cycle. Educators must design motivating learning environments to assist learners to acquire skills needed to achieve financial security. One approach is to view the audience through a generational lens. Several authors discuss using generational approaches in the workplace (Beattie, Rhoads, Staten, & Miller, 2005; Strauss & Howe, 1991), but few have discussed generational money management views.

Wuest, Welkey, Mogab, and Nicols (2008) discussed consumer decisions in a generational approach, stating that recognizing similarities and differences in generations is basic to understanding consumer behaviors. Each generation views money differently based on life and cultural experiences. Additionally, individuals may be affected by multi-generational financial issues such as aging parents, estate planning, business succession, and college and retirement savings. According to Joseph Hoffman, Institute of Certified Financial Planners (1999), "The issues often are complicated by the fact that people don't like to talk about their money and that different generations often view money and its use in different ways." In a 2007 focus group study, Millennial college students specified preferences for accessing financial information online or with a trusted individual, which is different from other generational cohorts (Hendrickson, Hagen Jokela, Gilman, Croymans, Marczak, Zuiker, & Olson, 2010).

Generations are influenced by their unique life stories. Teaching financial literacy involves financial concepts and tasks appropriate for various life stages. Sharing knowledge about one's economic life experiences across various generations increases the capacity of all to expand their financial knowledge.

A tool developed by Extension educators of the University of Minnesota Extension and University of Wisconsin Cooperative Extension addresses the complex financial issues family members face. Educators reviewed Financial Management Throughout Your Life (Goss, 1982), a publication developed to address financial tasks throughout the lifecycle. They found that although many financial tasks were still applicable, the point within the lifecycle at which the tasks were accomplished may differ. For example, with delayed marriage and childbearing, Gen X individuals may be dealing with financial tasks and concerns previously seen as twenty-something issues.

A generational approach provides a broad view of tasks and addresses methods for reaching each generation. Kaplan, Tsen, and Radhakrishna, (2003) believe an intergenerational perspective has great potential for enhancing Extension's programming, leading to rich learning experiences and significant program impact. Intergenerational programs represent an effective means to enrich the lives of individuals across the lifespan, while strengthening family support systems, and contributing to the social cohesion of communities (Kaplan, Forthun, & Kostelecky, 2008). Using the Teaching Financial Literacy Across the Generations tool, educators can plan teaching activities addressing specific generational financial issues, while also considering topics for multi-generational audiences. The tool examines generational characteristics, life cycle tasks, potential concerns, financial concepts, teaching techniques and activity examples.

Use of Tool to Plan Education

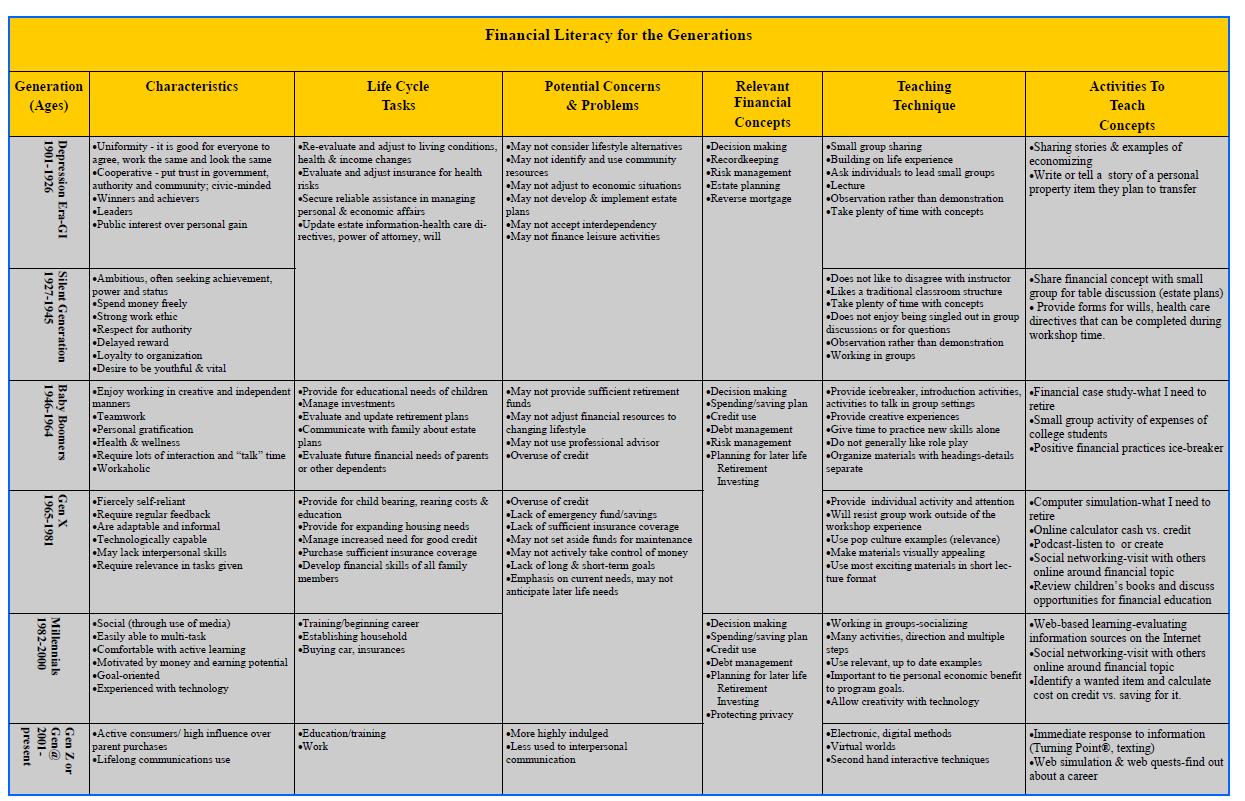

Figure 1.

Teaching Financial Literacy Across the Generation Tool

The following example illustrates how to use the tool. Boomers are quite generous in providing financial assistance to parents and children while potentially disregarding their own financial needs (Ameriprise Financial, 2007). When planning an educational session including Boomers, an educator may refer to the tool's chart to reflect on Boomer characteristics and appropriate teaching methods for this cohort:

- Generation: Baby Boomers: 1946-1964

- Characteristics: Enjoy working in creative and independent manners; Teamwork; Personal gratification; Health and wellness; Require lots of interaction and "talk" time; Workaholic

- Life Cycle Tasks: Provide for educational needs of children; Manage investments; Evaluate and update retirement plans; Communicate with family about estate plans; Evaluate future financial needs of parents or other dependents

- Potential Concerns and Problems: May not provide sufficient retirement funds; May not adjust financial resources to changing lifestyle; May not use professional advisor; Overuse of credit

- Relevant Financial Concepts: Decision making; Spending/saving plan; Credit use; Debt management; Risk management; Planning for later life: Retirement and Investing

- Teaching Technique: Provide icebreaker, introduction activities, activities to talk in group settings; Provide creative experiences; Give time to practice new skills alone; Do not generally like role play; Organize materials with headings-details

- Activities to Teach Concepts: Financial case study-what I need to retire; Small group activity of expenses of college students; Positive financial practices icebreaker

After reviewing Boomer information, the educator may select a case study discussing the competing financial interests Boomers experience and have groups brainstorm solutions. This allows for listening and learning from individuals representing different generations. Differing individual values and goals shared and discussed increase understanding of generational similarities and differences affecting life decisions.

Using a generational approach offers benefits, including increased opportunities for participant's contribution, confidence building, and understanding those of various ages and cultures (Kaplan, Forthun, & Kostelecky, 2008).

Additional examples include:

- A Depression era person sharing experiences with Millennials to highlight the importance of saving money.

- A Millennial and Silent relating struggles in the job market and comparing experiences.

- A Gen Z participant sharing online account management expertise with a Silent.

Results

In post- then pre-evaluations participants indicated that 95% either agreed or strongly agreed that they understood the importance of exploring ways to reach different generations and ideas to create active learning environments compared to 69% before the workshop.

Participant responses to the question, "As a result of the workshop, I plan to:

- "Spend more time recognizing different age groups of people I work with"

- "Integrate activities in financial planning"

- "The age group/learning style table is very helpful and I will share with schools across the southeast!"

A PowerPoint presentation and written publication have been shared through regional, state and national conferences.

Conclusion

When teaching financial concepts, it is important to consider participants' needs and interests. By providing a variety of experiences, life stories can be shared creating meaningful financial education, helping individuals internalize learning and applying to their own financial situations. Bowling and Brahm (2002) stated that bringing people together by reflecting on their experiences and creating shared knowledge can help align understanding across generations. By using the Teaching Financial Literacy Across the Generations tool, educators can compare generational financial concerns and create and deliver meaningful learning experiences, leading to long-term financial capability.

References

Ameriprise Financial. (2007). Money across generations study.

Beattie, S., Rhoads, A., Staten, A., & Miller, D. (2005). Teaching across generations. Effective Teaching & Learning Department.

Bowling, C., & Brahm, B. (2002). Shaping communities through Extension programs. Journal of Extension [On-line], 40(3). Article FEA2. Available at: http://www.joe.org/joe/2002june/a2.php

Goss, D. (1982). Financial management throughout your life. University of Minnesota Extension Service.

Hendrickson, L., Hagen Jokela, R., Gilman, J., Croymans, S., Marczak, M., Zuiker, V., & Olson, P. D. (2010). The viability of podcasts in Extension education: Financial education for college students. Journal of Extension [On- Line], 48(4). Article 4FEA7. Available at: http://www.joe.org/joe/2010august/a7.php

Hendrickson, L., Hagen Jokela, R., & Haynes, B. (2011). Teaching financial literacy across the generations. Poster session presented at the Association for Financial Counseling and Planning Education, Jacksonville, FLA.

Hoffman, J. (1999). Financial planning for the multigenerational family. Institute of Certified Financial Planners.

Kaplan, M., Forthun L., & Kostelecky, K. et al. (2008). Rationale and recommendations for strengthening the intergenerational agenda within Cooperative Extension. [White paper].

Kaplan, M., Tsen, S., & Radhakrishna, R. (2003). Intergenerational programming in Extension: Needs assessment as planning tool. Journal of Extension [On-line], 41(4). Article 4FEA5. Available at: http://www.joe.org/joe/2003august/a5.php

Strauss, W., & Howe, N. (1991). Generations: The history of America's future 1594 to 2069.

Wuest, B., Welkey, S., Mogab, J., & Nicols, K. (2008). Exploring consumer shopping preferences: Three generations. Journal of Family & Consumer Science 100(1).