October 2012

|

October 2012 // Volume 50 // Number 5 // Research In Brief // v50-5rb2

Family Resource Management Needs Assessment in New Mexico

Abstract

New Extension state specialists face many uncertainties when beginning to work in their new position, especially when it involves a state unfamiliar to them. Literature reviews may not provide the latest and clearest picture of the needs and challenges in the state. Furthermore, the between-county variation of issues may differ greatly. The study reported here illustrates how a survey of Home Economics county agents may benefit a new Extension specialist and provide a picture of Extension Home Economics needs and challenges specific to New Mexico.

Introduction

Surveying is one of the better ways a new Extension specialist can obtain the latest on county needs. A survey given to county agents has the advantages of serving as an icebreaker, potentially producing a better response (e.g., designed with anonymity), reaching out to respondents in a large geographical area, and obtaining the latest information from reliable sources. The need of a survey is especially true for a unique state like New Mexico (NM) and a diverse area such as Home Economics (Koukel & Cummings, 2003). Some 2009 statistics that make NM unique included a per capita personal income of $32,394, which ranked 43rd in the nation (Bureau of Economic Analysis, 2011); 18.0% of residents lived below the poverty level compared to 14.3% nationally (Bishaw, 2011); 40.6% of working families lived at poverty level, which ranked 49th in the nation (Working Poor Families Project, 2012); and 30% of the population were estimated to be functionally illiterate (New Mexico Coalition for Literacy, 2011) compared to 20% nationally (United Nations Development Programme, 2009).

Home Economics county agents (hereafter, Home Economists) in the 33 counties in New Mexico (2009 population: 2,009,671, Census, 2010a) are in charge of six main programs, namely Food & Nutrition, Food Technology, Family Life and Child Development, Family Health and Wellness, Diabetes, and Family Resource Management. In 2009, 10 counties did not have a specified Home Economist. Depending on needs and population, a few larger counties may have more personnel to handle related programs, while smaller ones may not have designated Home Economists. In some smaller counties, the county director assumes responsibility for these programs.

Examples of some 2009 programs and their impacts:

- 48 Kitchen Creations schools were conducted with 897 participants (New Mexico State University, 2010).

- 4,703 families were enrolled in Baby's First Wish/Just in Time Parenting newsletter program through September 2009 (Del Campo, 2009).

- 15,000 New Mexicans were impacted by Extension financial programs such as Jump$tart, quilting and craft workshops, and other family resource management programs (New Mexico State University, 2010).

- The Expanded Food and Nutrition Education Program (EFNEP) reached 929 adults and 2,053 youth (Turner, 2009).

Given the needs and constraints of organizing programs, a new Extension specialist may find it useful to conduct a needs assessment survey of the Home Economists in order to understand each county's needs and prioritize the programs offered. This is particularly true in the area of Family Resource Management, mainly consisting of the personal finance field, which encompasses savings, spending, budgeting, debt, home financing, retirement planning, investment, and credit cards. Because Home Economists deal directly with the public, surveying them is the most efficient way to gain the latest insights that represent various areas of New Mexico.

The main objectives of the study reported here were to understand financial and other family resource needs across the state of New Mexico, enhance the delivery of Family Resource Management programs, and show the advantages of a needs assessment survey, especially for new Extension Specialists. Specifically, the results of the survey identified Financial Resource Management needs and constraints for the state of New Mexico.

Methods

Instruments

A 22-item survey was designed to cover Home Economists':

- Involvement in various Home Economic programs (three items),

- Involvement and opinions on various Financial Resource Management programs and Specialist (seven items),

- Knowledge in Financial Resource Management areas (10 items) - Split-half reliability = 0.665, and

- Opinions on other miscellaneous topics (two items).

For the online survey, the seven main programs were collapsed into five. Diabetes and Food Technology were grouped with Food & Nutrition. Different questions utilized different scales, which included Likert scale, "select any," and "select the correct answer" questions. Among the 13 items for knowledge in Family Resource Management areas, 10 items tested Home Economists on the basics of Financial Resource Management, specifically personal finance. Almost all of these questions were taken from FINRA's (Financial Industry Regulatory Authority's) Investors Quiz (2007). For questions with nominal responses, response choices were randomly arranged to minimize bias due to response order appearance.

Procedure

The survey was developed using Zoomerang, an online survey tool. Home Economists and county agents responsible for Home Economics programs (for counties without a Home Economist) were solicited to participate via a Home Economist email listserv. (Note: From this point forward, "Home Economists" include county agents responsible for Home Economics programs.)

The email included the purpose, rationale, contact person, and Institution Review Board (IRB) permission form. The survey was open from September 2009 to January 2010. Other than the required questions, optional information on county name, respondent name, and academic major were asked.

Results

Nineteen county agents responded to the survey. The response rate was 57.5%. The counties in which these respondents served represent 69.6% of the New Mexico population. Using Fisher's exact test, there was only one significant difference out of 82 individual comparisons between Extension personnel who provided their names and those who did not: Food and Nutrition in program importance ranking (p = 0.0114). Because all but one comparison (1.2%) was significant, the results of the study were pooled, i.e., Extension personnel who provided their names and those who did not were not separated for comparisons.

Home Economics Programming

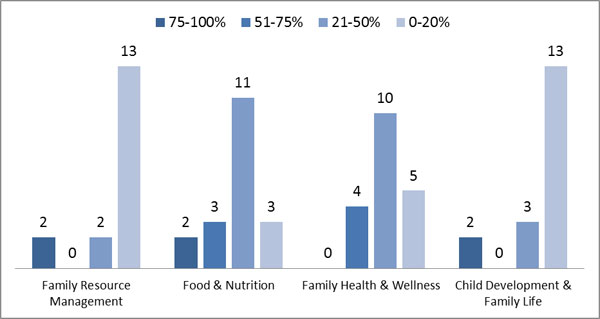

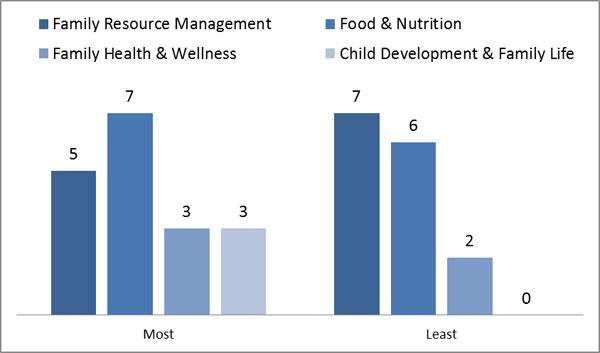

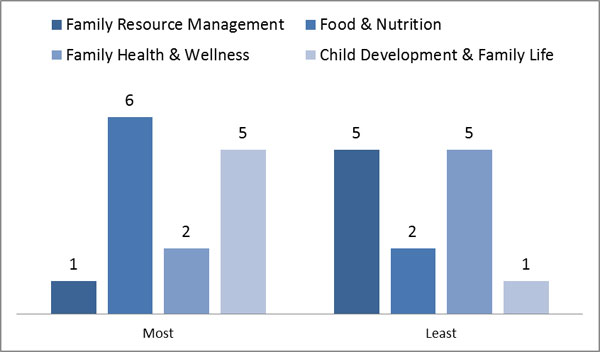

Figures 1, 2, and 3 summarize Home Economists' responses on time spent in the four main areas of Home Economics, the program most often conducted by Home Economists, and the most important programs, respectively.

As represented in Figure 1, Home Economists in New Mexico tend to spend more time in the areas of Food & Nutrition and Family Health & Wellness and less time in the areas of Family Resource Management and Child Development & Family Life. Five Home Economists reported spending more than 50% of their time on Food & Nutrition programs (26.3%), while four Home Economists reported the same for Family Health & Wellness (21.0%). Thirteen respondents (68.4%) reported spending less than 20% of their time on Family Resource Management and Child Development & Family Life.

Figure 1.

Time Spent in Home Economics Program Areas

As depicted in Figure 2, seven Home Economist respondents marked Food & Nutrition as the area with the most programs conducted (36.8%). Despite having the next highest responses (five) for the most programs conducted (26.3%), Family Resource Management also had the most responses for the program least often conducted in seven other responses (36.8%). The second least conducted were Food & Nutrition programs. Child Development & Family Life had the least responses for the programs most often conducted (three responses, 15.8%) but had zero response for the program least often conducted.

Figure 2.

Programs Most and Least Often Conducted

Figure 3 shows that when asked about program importance, Home Economists believed that the most important program area was Food & Nutrition with six responses (31.6%), closely followed by Child Development & Family Life with five responses (26.3%). Family Resource Management was the least important program among the ones listed based on it receiving fewer responses (one) to the question regarding the most important program and it receiving one of the highest responses (tied at 5) for the least important program question.

Figure 3.

Most & Least Important Programs

Family Resource Management Programming and Knowledge

When asked about reasons for not having more Family Resource Management programs, two reasons stood out with seven responses each: lower priority and complexity of Family Resource Management topics. The complexity of Family Resource Management topics was reflected in the 10-question quiz that was included in the survey. Among the 17 Home Economists who responded to a self-assessment on financial management, one self-assessed as "very good," nine as "good," six as "average," and one as "bad." This information was somewhat evident from the uniform distribution of the 10-item quiz scores (mean = 4.9, standard deviation = 2.95, median = 5, minimum = 0, maximum = 9). Among the 10 questions asked, high scores (>70% correct) were recorded for questions on credit cards, payday lending, disposable income, and net worth. On the other hand, low scores (<50%) were observed for questions on investment and retirement planning.

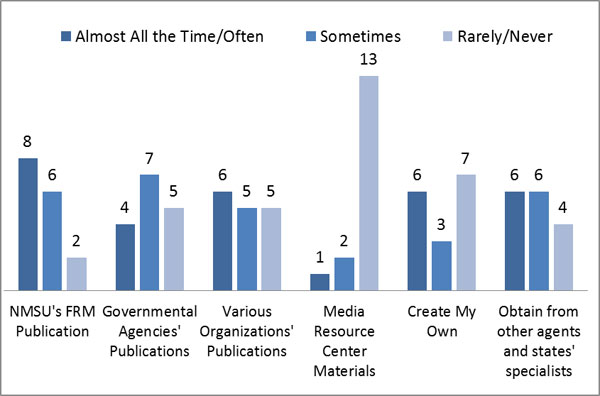

As for highly needed Family Resource Management programs, money management had the most responses, by far, at 15 (79%), followed by payment methods such as credit cards (11 responses), consumer protection (10 responses), home energy (10 responses), savings (9 responses), mortgage (8 responses), retirement (7 responses), and finance for youth (6 responses). As portrayed in Figure 4, there was no single resource employed by Home Economists for Family Resource Management programs. NMSU's Family Resource Management (FRM) publication shows the highest usage among the categories presented with eight "almost all the time/often" responses (42.1%). The next highest usage categories are three that tied with six "almost all the time/often" responses (31.6%): Various Organizations' Publications, Create My Own, and Obtain from other agents and states' specialists. The highest number of responses for one category was 13 (68.4%) "rarely/never" responses for the use of the Media Resource Center of NSMU Extension Home Economics Department, with resources estimated at about $200,000.

Figure 4.

Utilization of Resources When Preparing for Family Resource Management Programs

County Agent-Specialist Communication and Other

When asked about qualities that were important for a Family Resource Management specialist to have, an overwhelming 14 respondents (73%) responded with "strongly agree" with regards to communication, while the rest (three) responded with "agree," as shown in Table 1. Also high in the "strongly agree" category were working together with Home Economists (11 responses), producing up-to-date "How To" publications, providing more clinics to train Home Economists (10 responses), and presentation skills (nine responses). Mastering of Spanish and Native Indian languages had the most "strongly disagree" or "disagree" with five responses. When asked about better means of communication, the best ones were on-site training (eight "best," five "good"), email (five "best," eight "good"), and online training (four "best," seven "good"). Telephone has seven "good" responses, but only one "best" response. Online chatting has eight "indifferent/ok" responses.

| Qualities | Mean (Standard deviation) | Strongly Agree | Agree | Neutral/ Indifferent | Strongly Disagree or Disagree |

| Local Languages | 2.8 (1.05) | 1 | 2 | 8 | 5 |

| Presentation Skills | 4.5 (0.51) | 9 | 8 | 0 | 0 |

| Networking | 4.2 (0.91) | 7 | 6 | 2 | 1 |

| Grant Funding | 3.9 (0.86) | 4 | 8 | 4 | 1 |

| Communication | 4.8 (0.4) | 14 | 3 | 0 | 0 |

| Computer Skills | 4.1 (0.57) | 3 | 11 | 2 | 0 |

| Working with Agents | 4.65 (0.49) | 11 | 6 | 0 | 0 |

| "How To" Publications | 4.5 (0.72) | 10 | 5 | 2 | 0 |

| Training | 4.5 (0.72) | 10 | 5 | 2 | 0 |

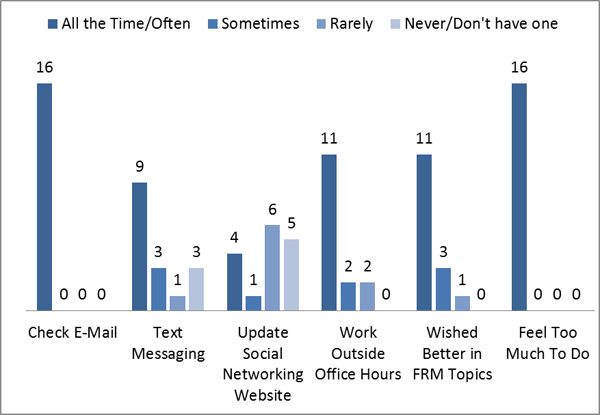

Figure 5 shows responses to miscellaneous questions on Home Economists' routines. Sixteen (84%) Home Economists responded that they check email "often" or "all the time," and the number reported encountering situations where there is too much to do "often" or "all the time." Most of the respondents (11) do not have or rarely update social networking sites (e.g., Facebook, Friendster, MySpace, LinkedIn), but many of them (nine) send text messages via phone "all the time" or "often." Most of them (11) reported working outside of office hours "always" or "sometimes."

Figure 5.

How Often Do You … ?

Discussion and Implications

Usefulness of Needs Assessment

This article illustrates the benefits of surveying county agents for a state needs assessment and insight on the latest trends in Extension Home Economics programs in New Mexico. Besides the needs area, the survey has provided quick and rich information about agents' opinions, knowledge on personal finance topics, educational background, and main challenges in conducting Family Resource Management programs. This information is especially valuable to new specialists attempting to tailor their county's programs accordingly.

Although the study was based on New Mexico counties, its importance, results, and methods are applicable to the national Extension Home Economics or Family Consumer Sciences programs. Home Economists in many states are expected to conduct programs in the diverse areas of Home Economics without being well versed in these areas, especially in personal finance. Expected to deliver basic personal finance programs, Home Economists did not fare well in the 10-questions quiz provided. A similar trend was observed nationally for teachers who were responsible for teaching personal finance (Way & Holden, 2009). In addition, the tendency of Home Economists to gravitate towards Food & Nutrition and Family Health & Wellness programs was also observed at the national level (Branan & Rohs, 1991; Murphy, Coleman, Hammerschmidt, Majewski, & Slonim, 1999).

Personal Resource Management Extension Programs

The need for adequate Family Resource Management programs is very high given the economic crisis. This is especially true for women, who are the main clients for Home Economists. Women cannot sit back and expect their spouses or parents to handle their personal finances as in the past. As many as 90% of women will need to be in charge of their own financial management at some point in their lives (Brennan & O'Neill, 2004) due to not marrying, a shorter life expectancy trend, and a higher divorce rate. This is disconcerting because women tend to perform poorly when it comes to financial literacy questions (Lusardi & Mitchell, 2007) and receive lower pension income. In addition, Brennan and O'Neill (2004) noted that women tend to get paid 25% less than their male counterparts and spend 11 years out of the workforce due to giving birth to and caring for children, as well as caring for frail elderly.

Because Family Resource Management topics can get complicated, Home Economists may also utilize other approaches to increase necessary Family Resource Management programs. These approaches include inviting professionals to provide assistance in Financial Resource Management programs for highly complex topics, collaborating with other organizations, purchasing curriculum with visual presentations, and relying on online Extension resources (Pankow & O'Neill, 2008; Muske, Goetting, & Vukonich, 2001). Another approach is to improve marketing to agents on the resources available at the university, such as the Media Resource Center, where much Extension Home Economics educational material is housed. Home Economists who are more knowledgeable in personal finance may assist other Home Economists in neighboring counties for Family Resource Management programs, like those employed in other states such as Idaho and Indiana. However, unlike these two states, New Mexico's counties tend to be larger with no county agent to specifically focus on personal finance education.

Working Together and Communication

The top two qualities of a Financial Resource Management specialist desired by Home Economists were improved communication and working relations. Based on the survey, the best ways to communicate with Home Economists were via e-mail and telephone. Social Media means may not be the best way to share regular news feed such as the latest news, product recall, and educational program updates. The potential for Home Economists to adopt this type of media exists based on online purchasing and for-personal Social Media utilization. The current lack of Social Media utilization for work is likely to be related to low Internet access (U.S. Census, 2010b), the functional illiteracy rate (New Mexico Coalition for Literacy, 2011), and having too much to do at work.

In promoting programs to Home Economists, specialists need to keep in mind that Home Economists already have many things on their plate (Ensle, 2005). In the study reported here, Home Economists reported working outside office hours and having too much to do, and almost half of them reported creating their own Family Resource Management program. Thus, specialists' approaches need to include marketing available programs to the Home Economists; lending assistance to improve programs created by Home Economists (if needed); and focusing on short and simple financial education topics. Money management programs should be considered due to an almost complete consensus of its need by the Home Economists surveyed.

These needs assessment results have been useful in designing effective Family Resource Management programs to suit county needs and Home Economists preferences. Examples of this include:

- Focusing on simple and short personal finance programs such as budgeting, Dollar Decision$, and the High School Financial Planning Program;

- Communicating extensively via email and phone for important news while establishing presence via the informative Family Resource Management website, Twitter®, Facebook®, and SlideShare®; and

- Taking programs created by Home Economists to another level by improving evaluation components, applying for grants, and presenting these programs in national conferences.

References

Bishaw, A. (2011). Poverty: 2009 and 2010, American Community Survey Briefs, ACSBR/10-01. U.S. Census Bureau. Retrieved from: http://www.census.gov/prod/2011pubs/acsbr10-01.pdf

Branan, S., & Rohs, F. R. (1991). Home Economists identify research needs. Journal of Extension [On-line], 29(2) Article 2RIB3. Available at: http://www.joe.org/joe/1991summer/rb3.php

Brennan, P.Q., & O'Neill, B. (2004). Money Talk: A financial guide for women. Ithaca, NY: Natural Resource, Agriculture, and Engineering Service.

Bureau of Economic Analysis (2011). SA1-3 - personal income summary table. U.S. Department of Commerce. Retrieved from: http://www.bea.gov/regional/spi/drill.cfm

Del Campo, D. (2009). Age paced parenting newsletters: New Mexico's baby's first wish and e-Xtension's just in time parenting. Plan of Work 2009, New Mexico State University. Retrieved from: http://pow.nmsu.edu/view_plan.php?plan_id=595

DeNavas-Walt, C., Proctor, B. D., & Smith, J. (2008). Current population reports, P60-235, Income, poverty, and health insurance coverage in the United States: 2007. U.S. Census Bureau , U.S. Government Printing Office, Washington, DC.

Ensle, K. E. (2005). Burnout: How does Extension balance job and family? Journal of Extension [On-line], 43(3) Article 3FEA5. Available at: http://www.joe.org/joe/2005june/a5.php

FINRA (2007) Investor knowledge quiz. Retrieved from: http://apps.finra.org/quiz/1/investorquiz.aspx

Koukel, S. D., & Cummings, M. N. (2003). New Mexico Cooperative Extension Service Home Economists' perceived technical knowledge and estimated client needs. Journal of Extension [On-line], 40(5) Article 5FEA5. Available at: http://www.joe.org/joe/2002october/a5.php

Lusardi, A., & Mitchell, O. (2007). Financial literacy and retirement preparedness. Evidence and implications for financial education. Business Economics, January 2007, 35-44.

Murphy, A., Coleman, G., Hammerschmidt, P., Majewski, K., & Slonim, A. (1999). Taking the time to ask: An assessment of Home Economics Agents' resource and training needs. Journal of Extension [On-line], 37(6) Article 6RIB3. Available at: http://www.joe.org/joe/1999december/rb3.php

Muske, G., Goetting, M. & Vukonich, M. (2001). The World Wide Web: A training tool for Family Resource Management educators. Journal of Extension [On-line], 39(4) Article 4FEA3. Available at: http://www.joe.org/joe/2001august/a3.php

New Mexico Coalition for Literacy (2011) Governor Susana Martinez declares literacy day throughout the state of New Mexico [Press release]. Retrieved from: http://www.nmcl.org/MainSite/AllFiles/PDFs/Press%20Release%209.2.11.pdf

New Mexico State University (2010). 2009 New Mexico State University combined research and Extension annual report of accomplishments and results. Retrieved from: http://aces.nmsu.edu/aes/planofwork/docs/2009%20AREERA%20Annual%20Report%20of%20Accomplishments%20and%20Results.pdf

Pankow, D., & O'Neill, B. (2008) eXtension financial security for all: A community of practice to increase financial literacy. Journal of Extension [On-line], 40(5) Article 5FEA5. Available at: http://www.joe.org/joe/2008june/a3.php

Turner, C. (2009) KA 703. Nutrition education and behavior. Plan of Work 2009, New Mexico State University. Retrieved from: http://pow.nmsu.edu/view_plan.php?plan_id=7&page=28

U.S. Census Bureau (2010a). 2009 American community survey 1-year estimates, 2009 American Community Survey. Retrieved from: http://factfinder.census.gov/

U.S. Census Bureau (2010b) Reported Internet usage for individuals 3 years and older, by state based on Current Population Survey (CPS) Supplement 2009, Table 3.. Retrieved from: http://www.census.gov/hhes/computer/publications/2009.html

United Nations Development Programme (2009). Human development report 2009. New York, NY. 2009. Retrieved from: http://hdr.undp.org/en/media/HDR_2009_EN_Complete.pdf.

Way, W. L., & Holden, K. C. (2009). Teachers' background and capacity to teach personal finance: Results of a national study. Journal of Financial Counseling and Planning Education, 20(2), 64-78.

Working Poor Families Project (2012). Conditions of low-income working families. Retrieved from: http://www.workingpoorfamilies.org/xls/2011WPFP_Conditions_Low-Income_Working_Families.xls