February 2009

|

February 2009 // Volume 47 // Number 1 // Tools of the Trade // v47-1tt3

Consumers Ask: Should I Purchase Long-Term Care Insurance?

Abstract

Seventy million baby-boomers may face the need for long-term care (LTC). Therefore, educating them about long-term care insurance (LTCI) is necessary considering the high costs of LTC services and the aggressive marketing of LTCI by companies. It is important that consumers receive unbiased information regarding LTCI and how it fits into their personal financial situation. Seminars using the Should I Purchase Long-Term Care Insurance? presentation and accompanying Comparing Long-Term Care Insurance worksheet have helped Idahoans: (1) become more knowledgeable about LTCI, (2) decide if LTCI is right for them, and (3) learn how to effectively shop for and compare LTCI.

Introduction

A pressing question facing many of the 70 million American baby-boomers is whether or not to purchase long-term care insurance (LTCI). Recently, the oldest members of this generation reached 62 years of age. Due to technological advances and healthier lifestyles, baby-boomers are expected to live longer than any previous generation in history. However, boomers will also be facing higher costs than ever before for long-term care services and facilities. With current nursing home rates of $77,745/year for a private room, $68,985/year for a semi-private room, and $35,628/year for an assisted living facility (Metlife Mature Market Institute, 2007), these costs can quickly deplete an individual's assets.

Long-term care insurance has been available since the 1980's and is now a multi-billion dollar industry. More than 100 companies offer coverage, some of which have decades of LTCI experience, while others are relatively new to the LTCI business (American Health Insurance Plans, 2004). Depending on which policy options are selected and the individual's age when the policy is purchased, premiums for LTCI can vary considerably and can be very expensive (Lown & Palmer, 2004). Additionally, agent commissions can significantly add to the cost of LTCI. Consumer Reports states "agents can reap hefty commissions-50 percent of your first year's premium and 10 percent of your payment for every succeeding year" (Consumer Union, 2003).

LTCI is a fairly new type of insurance, and underwriters are still negotiating effective premium levels. There have been several insurance companies that have had to raise their customer's LTCI premiums anywhere from 10% to well over 100%. Premium increases and the ability to pay for the years until long-term care services may be needed are big factors in an individual's overall financial picture.

Purchasing LTCI is an important decision and should not be taken lightly because of costly premiums and the chance that a person could be paying premiums for 30+ years before needing the coverage. The average age of those admitted to nursing homes is 83 (Consumer Union, 2003). LTCI policy owners often become unable to keep up with increasingly expensive premiums that can significantly rise from when the policy was originally purchased to the time the benefits are actually used (Lown & Palmer, 2004). Consumers who purchase LTCI give up the other potential uses of the money spent on insurance premiums (Gold, Vanderlinden, & Herald, 2006). Many consumers run the risk of letting their policy lapse if they purchase LTCI during their working years and fail to consider the affordability of premiums after retirement (Lown & Palmer, 2004).

Unlike car and home insurance, LTCI is not easy to change or replace because it is underwritten based on the age and health of the applicant. LTCI also differs from other major types of insurance and can pose more risk to consumers because the consumer makes a long-term commitment to one LTCI company (Everett, Anthony, & Burkette, 2005). Some consumers are buying LTCI without fully assessing their financial situation and how LTCI will affect their overall financial planning for later life. It is vital that consumers perform an analysis of their retirement and non-retirement funds, before considering a LTCI purchase (Lown & Palmer, 2004).

Considering the rising costs of potentially necessary long-term care services and the expense of LTCI premiums, the decision to purchase LTCI can be complex, overwhelming, and confusing to consumers. Additionally, they are often bombarded with persuasive literature by sales professionals and can easily be misled into policies that are less than ideal for their given situations. (Lown & Palmer, 2004). When it comes to the wide assortment of benefits, costs associated with the policy, and features offered, LTCI policies can differ dramatically from one company to another. There is little help available for consumers to find unbiased information or guidance to assist them on how to compare LTCI policies during the decision-making process (Kassner, 2006).

Our Response

To prepare Idaho consumers to make educated decisions regarding LTCI, University of Idaho Extension, in cooperation with AARP-Idaho, developed the Should I Purchase Long-Term Care Insurance? presentation. The goal of the presentation is to provide Idaho consumers with unbiased information to help them determine if LTCI is right for them and, if yes, how to effectively compare and shop for LTCI. An accompanying Comparing Long-Term Care Insurance worksheet was developed and provided to the workshop participants. The worksheet is a tool to compare and shop for LTCI by completing a side-by-side comparison of policies. If they already own LTCI, information is offered on how to reevaluate their policy to make sure it fits their needs.

Should I Purchase Long-Term Care Insurance? presentation topics include:

- What LTCI is and when it should and should not be considered

- How to determine if LTCI is right for you,

- Steps to follow in evaluating a policy (even if you currently own a LTCI policy),

- Where LTCI can be purchased and how much it costs, and

- How to customize a policy that is right for you.

Seminar Outcomes

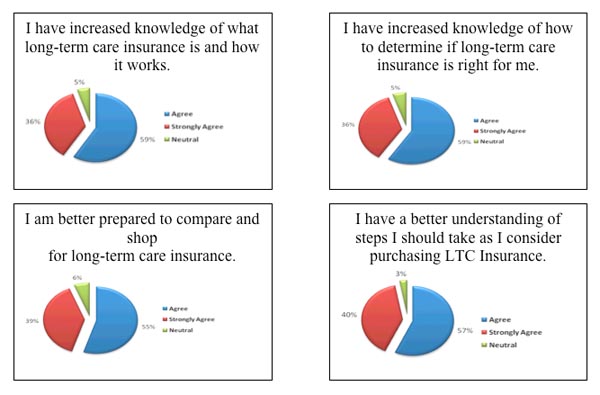

From 2005 to 2007, more than 700 Idahoans have attended 13 University of Idaho Extension Long-Term Care Seminars, co-sponsored by AARP-Idaho. At each seminar, Should I Purchase Long-Term Care Insurance? was presented. In post-evaluation surveys, participants were asked to rate their level of agreement on a five-point scale (strongly agree, agree, unsure/neutral, disagree, strongly disagree). Outcomes from 493 evaluations (62% Response Rate) are shown in Figure 1.

Figure 1.

Should I Purchase Long-Term Care Insurance? Evaluation Results

Furthermore, participants made comments like the following.

- "Wish I had been able to attend this workshop 15 years ago!"

- "It was worth the time spent and the trip made!"

- "Great presentation on a subject not easily understood."

- "Excellent, informative, timely, well presented and well-documented."

- "Didn't feel pressured to be with or without long-term care insurance."

Conclusion

The Should I Purchase Long-Term Care Insurance? presentation and accompanying Comparing Long-Term Care Insurance worksheet have helped Idaho's consumers: (1) become more knowledgeable about LTCI, (2) decide if LTCI is right for their personal financial situation, and (3) know how to effectively shop for and compare LTCI. This approach to educating consumers about LTCI has proven to be effective in Idaho.

References

America's Health Insurance Plans (2004). Guide to long-term care insurance. Retrieved March 3, 2008, from: http://www.pueblo.gsa.gov/cic_text/health/ltc/guide.pdf

Consumers Union (2003). Do you need long-term-care insurance? Consumer Reports, 68(11), 20-24.

Everett, M., Anthony, M., & Burkette, G. (2005). Long-term care insurance: benefits, costs, and computer models. Journal of Financial Planning [On-line], 7, 1-11. Retrieved March, 3, 2008, from: http://www.fpanet.org/journal/articles/2005_Issues/jfp0205-art7.cfm

Gold, J., Vanderlinden, D., & Herald, J. (2006). The financial desirability of long-term care insurance versus self-insurance. Journal of Financial Planning [On-line], 7, 144-149. Retrieved March, 3, 2008, from: http://www.fpanet.org/journal/articles/2006_Issues/jfp1106-art7.cfm

Kassner, E. (2006). Comparing long-term care insurance policies: bewildering choices for consumers. AARP Public Policy Institute In BRIEF, INB 125. Retrieved March, 3, 2008, from: http://www.aarp.org/research/longtermcare/insurance/inb125_ltci.html

Lown, J., & Palmer, L. (2004). Long term care insurance purchase: an alternative approach. Financial Counseling and Planning Journal, 15, 1-11.

Metlife Mature Market Institute (2007, October). The Metlife market survey of nursing home & assisted living costs 2007. Retrieved February 25, 2008, from: http://www.metlife.com/FileAssets/MMI/MMIStudies2007NHAL.pdf